This 12 months marks the 12 months of the stablecoin, particularly within the US. From the beginning of the 12 months, we’ve watched as stablecoins developed from an idea in trials abroad to a market drive attracting billions in each day transaction quantity, partnerships with main fee networks, lively pilots amongst US banks, and a central focus of US monetary regulation within the type of the GENIUS Act.

After the passage of the GENIUS Act in July, Ernst & Younger’s (EY) technique consulting providers group EY-Parthenon surveyed greater than 350 executives from monetary and nonfinancial sectors about their views on stablecoins. Based mostly on its findings, the agency generated a 31-page report that highlights adoption, utilization, advantages, challenges, regulatory implications, and extra. We’ve highlighted the report’s 5 main takeaways beneath.

Stablecoins are now not fringe

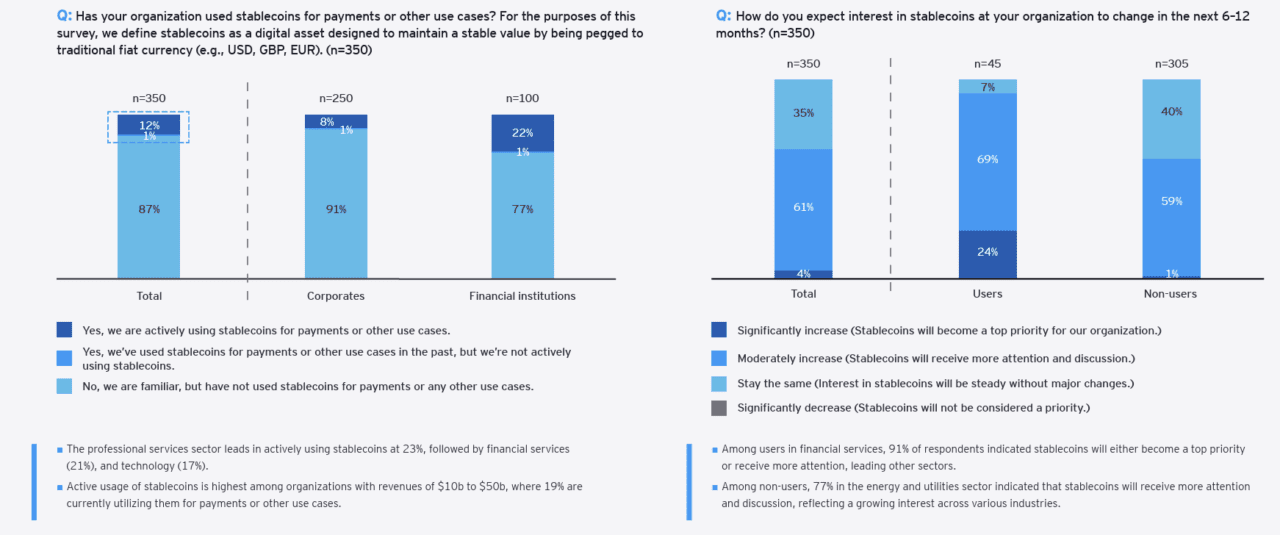

All the 350 executives surveyed are conscious of stablecoins. Of these, 13% have already used stablecoins and 65% anticipate curiosity in stablecoins to rise within the subsequent 6 to 12 months.

The truth that 100% of executives surveyed are conscious of stablecoins demonstrates how shortly stablecoins have moved into the mainstream. For banks and corporates, the dialog round stablecoins is now not a query of “if,” however moderately “how briskly” adoption spreads and what function the group ought to play. This shift from area of interest to norm exhibits that establishments that wait to make a transfer could miss out on shaping requirements and capturing early market share.

Charts from EY-Parthenon

Stablecoin utilization

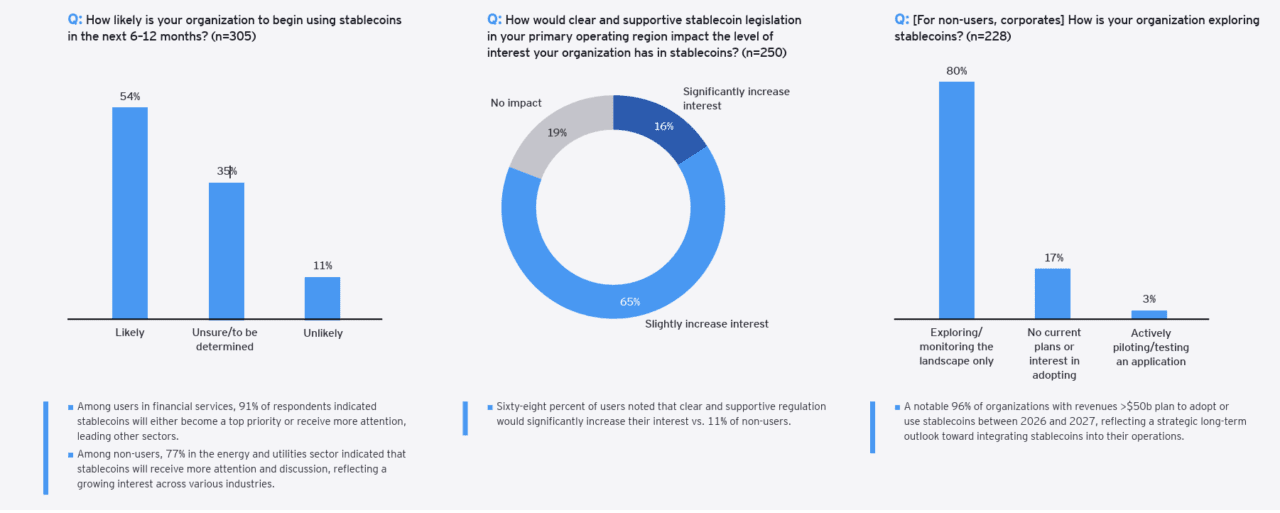

Greater than half, 54%, of monetary establishments and corporates that aren’t utilizing stablecoins anticipate to start utilizing them within the subsequent 6 to 12 months. For 81% of individuals surveyed, clear and supportive laws will increase their curiosity in stablecoins, both considerably or barely.

With greater than half of corporations signaling plans to undertake stablecoins inside a 12 months, the market will possible see an acceleration in utilization. For policymakers, this highlights the significance of regulatory readability, provided that it will straight increase adoption. For banks, it exhibits a possibility to deepen their relevance by providing compliant, stablecoin-enabled providers earlier than rivals get there first.

Charts from EY-Parthenon

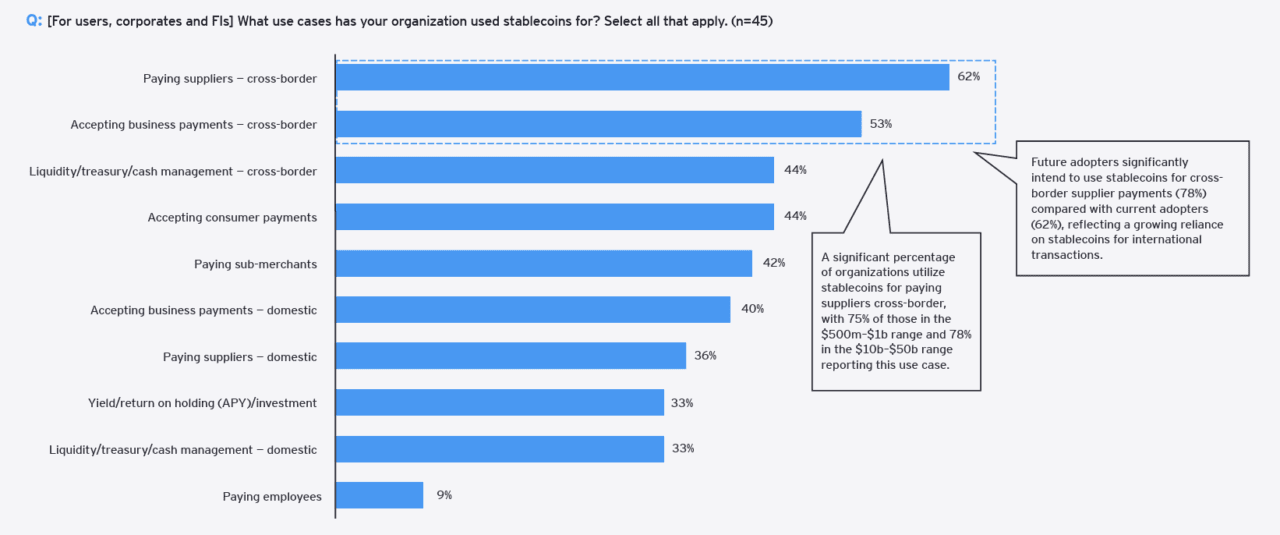

Cross-border fund transfers are the highest use case

The survey requested about 10 totally different use circumstances. Of these ten, the highest three use circumstances centered round cross-border funds.

This exhibits that stablecoins are tackling actual, persistent ache factors, particularly in cross-border funds. Regardless of earlier disruption by various gamers equivalent to Sensible, Remitly, and Revolut, worldwide transfers stay sluggish and costly. Stablecoins are a reputable various that resonates with companies and shoppers. This focus may disrupt entrenched correspondent banking networks and provides stablecoin adopters an edge within the profitable area of cross-border funds.

Charts from EY-Parthenon

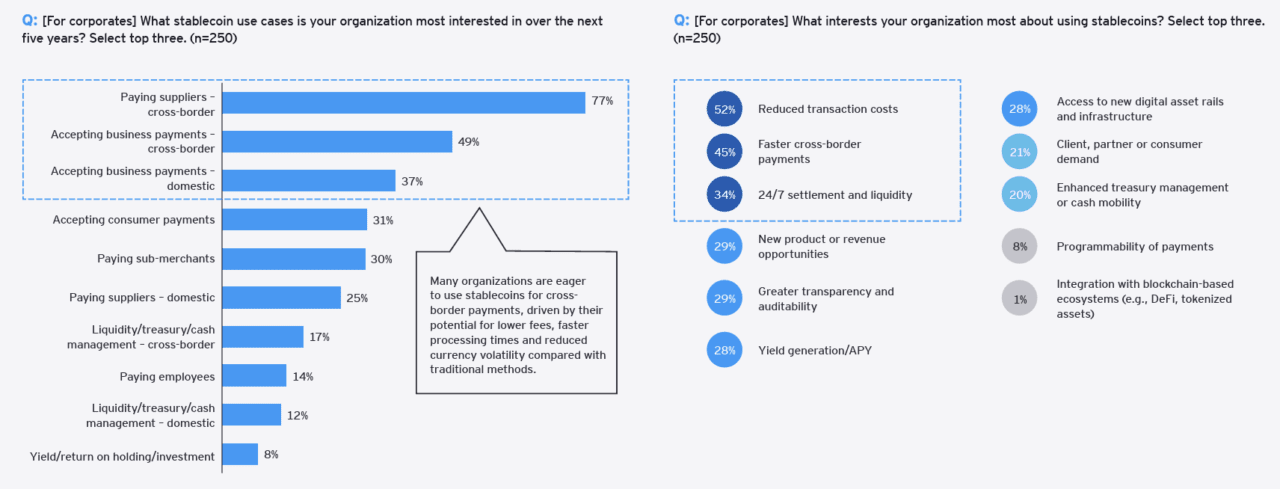

Corporations most considering lowering value and growing fee pace

Probably the most fascinating use case is cross-border funds (77%), with curiosity largely pushed by discount in transaction prices and quicker funds.

The overwhelming curiosity in value financial savings and pace is a reminder that stablecoins will succeed or fail based mostly on tangible worth, not hype. For companies, even modest reductions in cross-border charges can translate into important financial savings at scale. Banks face the problem of turning this effectivity right into a aggressive benefit, providing higher pricing and quicker settlement whereas managing dangers.

Charts from EY-Parthenon

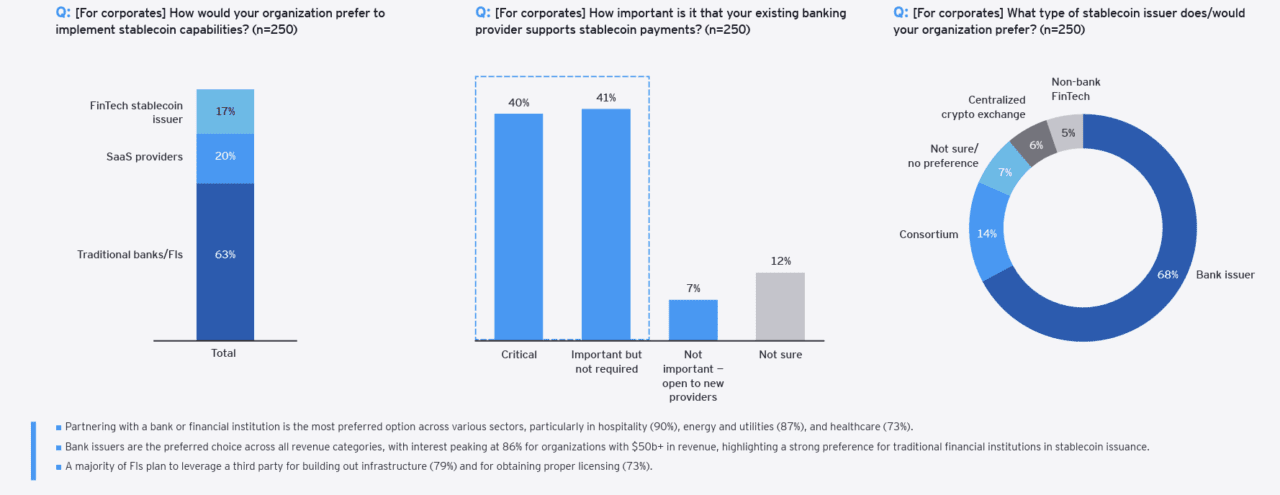

Sensible implementation

The survey discovered that organizations wish to their conventional banking companions for entry to stablecoins, and that the majority monetary establishments, 79%, plan to leverage a 3rd get together for stablecoin infrastructure.

The discovering that the majority organizations plan to entry stablecoins by way of present banking companions is critical. It suggests that companies need entry to stablecoins with out having to take care of the complexity that comes with the brand new fee rail. As a substitute of investing in-house to leverage the brand new expertise, they’re seeking to trusted intermediaries like banks to deal with the heavy lifting of facilitating the infrastructure. For banks, that is each a possibility and a warning. Establishments that transfer shortly to construct dependable, third-party-powered stablecoin providers can strengthen shopper relationships, whereas laggards danger being bypassed fully.

Charts from EY-Parthenon

Picture by Sebastian Svenson on Unsplash

Views: 19

Crypto Plan — Is Bitcoin Retirement Coming?")

{kind=link}