In July of 2025, the GENIUS Act, the primary complete federal framework for stablecoins, turned legislation. Final week, the US Workplace of the Comptroller of the Foreign money (OCC) issued a discover of proposed rulemaking (NPRM) to implement the GENIUS Act’s necessities for fee stablecoin issuance and associated actions.

Whereas the brand new proposed rulemaking makes the GENIUS Act a actuality as an alternative of only a statute, it doesn’t change the intent of the GENIUS Act. It operationalizes the GENIUS Act by making a devoted regulatory part for issuers, establishing the licensing mechanics and timelines, forming the capital and operational necessities, and stipulating overseas issuer therapy.

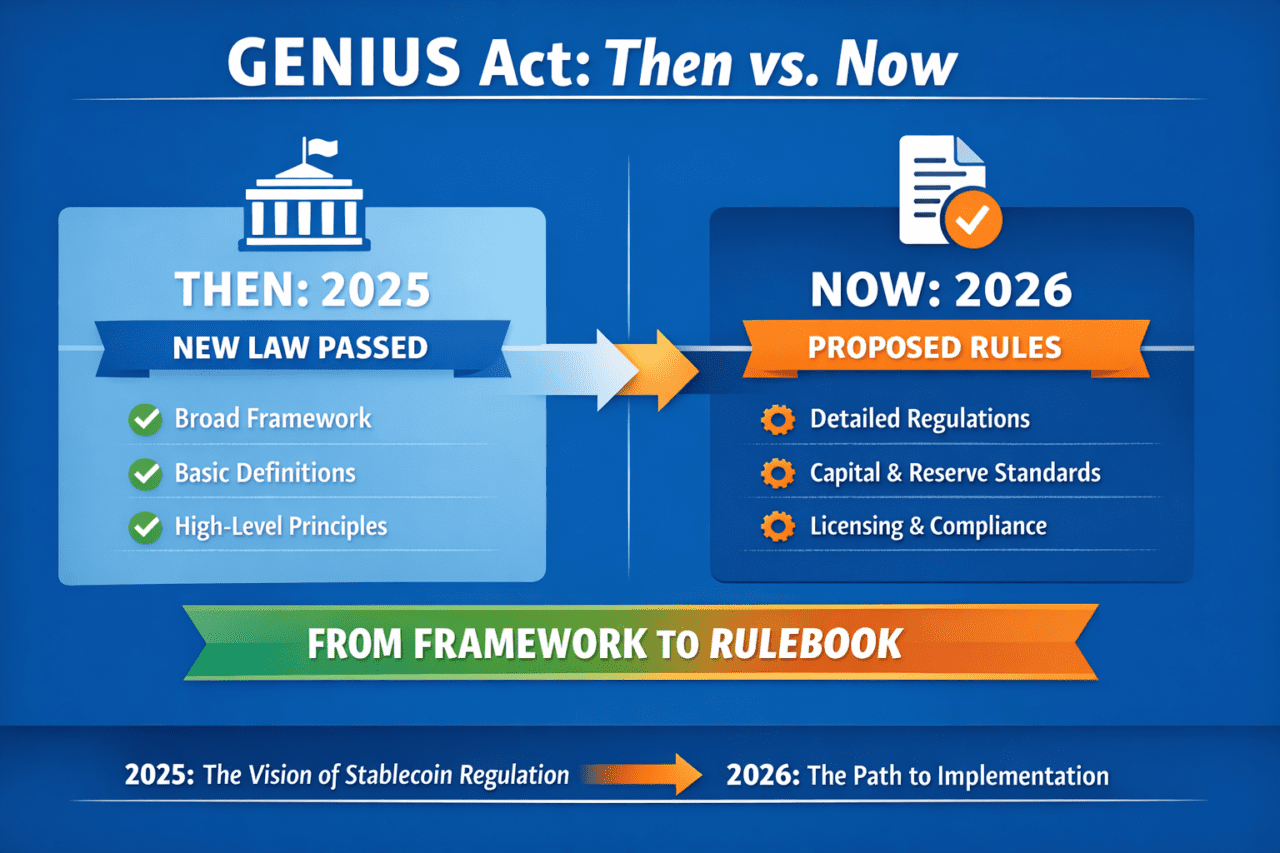

2025 GENIUS Act

The 2025 GENIUS Act had an important position in setting the stage for the legality of stablecoin funds. It outlined what a fee stablecoin is and who’s allowed to difficulty stablecoins. It stipulated that stablecoins require full reserve backing with liquid property, prohibited interest-bearing stablecoins, and created a federal and state regulatory construction. Total, the aim of the 2025 Act was to set guardrails. With this yr’s discover of proposed rulemaking, the OCC is bringing a extra procedure-focused method.

New devoted regulation

As talked about above, the OCC is operationalizing the GENIUS Act in 4 main methods, the primary of which creates a devoted regulatory part (12 CFR Half 15) that establishes requirements and necessities for stablecoin issuers. Creating the brand new half within the CFR modifications the GENIUS Act from a written requirement into extra enforceable supervisory requirements.

New licensing

Moreover, new licensing mechanics come into play that create an outlined pathway for coming into the stablecoin market. Below the OCC’s proposal, potential permitted fee stablecoin issuers (PPSIs) should submit a proper software outlining their enterprise mannequin, governance construction, reserve administration method, expertise infrastructure, and threat controls. The proposal establishes what constitutes a “considerably full” software and descriptions supervisory evaluate expectations. The brand new licensing course of makes stablecoin issuance just like making use of for a financial institution constitution, somewhat than launching a brand new product.

New capital and operational necessities

Equally, the 2026 capital and operational necessities make stablecoin issuance look extra like operating a regulated monetary establishment than launching a brand new product. Whereas the 2025 GENIUS Act centered totally on reserve backing, the OCC’s 2026 proposal stipulates minimal capital thresholds, liquidity buffers past token redemption obligations, formal governance buildings, inner management requirements, and express third-party threat administration expectations.

Established banks have already got these processes embedded into their working procedures. For fintechs, nonetheless, the brand new necessities might name for significant funding in governance, compliance documentation, and threat oversight infrastructure. These new formalities elevate the price of entry into the stablecoin issuance market.

New overseas issuer therapy

The OCC’s 2026 proposal incorporates overseas issuer guidelines straight into the scope of the plan, that means that non-US gamers can now not depend on regulatory ambiguity as a method to enter the market.

Simply because the proposed framework requires US issuers, overseas issuers serving US customers would nonetheless be required to use for OCC registration, present proof of Treasury’s comparability willpower, consent to US jurisdiction and OCC entry to information, and meet necessities round US-available reserves (topic to any reciprocal association).

This limits offshore entities working in regulatory grey zones whereas advertising and marketing to US prospects. The brand new rulemaking makes clear that world stablecoin gamers might want to align with US supervisory expectations, making a extra demanding roadmap for cross-border participation.

What this implies for banks and fintechs

The proposed rulemaking makes clear that stablecoins are shifting nearer to the core of regulated banking exercise and are more and more being handled as a part of the monetary infrastructure somewhat than as a crypto experiment. As stablecoin issuance begins to resemble supervised exercise, banks enter the dialog from a place of structural benefit. With governance frameworks, capital planning, threat administration, and compliance processes already embedded of their working fashions, conventional monetary establishments could also be higher positioned than fintechs to adjust to the regulatory calls for of stablecoin issuance.

As compliance prices related to stablecoin issuance rise, so does the barrier to entry. Not each fintech could have the urge for food or assets to satisfy capital, liquidity, and supervisory expectations. The elevated friction, nonetheless, brings institutional credibility to a fee kind as soon as thought of adjoining to Bitcoin. This credibility lowers the danger for issuers in addition to for finish customers and can in the end remodel stablecoins into an on a regular basis device.

Photograph by Moose Photographs

Views: 28

{kind=link}