FICO inventory has been crushed, falling greater than 50% from its highs. The Every day Breakdown digs into to see what’s occurring.

Earlier than we dive in, let’s be sure to’re set to obtain The Every day Breakdown every morning. To maintain getting our day by day insights, all you could do is log in to your eToro account.

Deep Dive

Truthful Isaac Company — ticker image “FICO” — operates in two most important segments: Software program, which offers decision-management options and the modular FICO Platform, and Scores — an idea shoppers are doubtless extra aware of — which delivers credit-scoring merchandise to companies and consumer-facing scores by myFICO.com subscriptions.

The corporate has confronted a brutal one-two punch, as AI disruption worries and elevated aggressive strain have culminated within the inventory’s pummeling. Shares have fallen 26% this week alone and are down greater than 50% from the document excessive in December 2024.

Regardless of the inventory’s tumble, the basics have been holding up:

Discover how income (blue) and earnings (orange) proceed to pattern increased, whereas estimates for fiscal 2026 and 2027 additionally level to additional development. In the meantime, working margins (purple) have been drifting increased over time and have — no less than to date — averted being squeezed decrease, which is a most important concern amid AI disruption and aggressive considerations.

Future Progress Projections

In accordance with Bloomberg, analysts challenge the next:

Earnings Progress: 40% in 2026, 26.7% in 2027, and 18.7% in 2028

Income Progress: 25.5% in 2026, 16.8% in 2027, and 12.5% in 2028

Analysts presently have a consensus worth goal of ~$2,068 on FICO inventory, implying about 87% upside to at this time’s inventory worth.

Need to obtain these insights straight to your inbox?

Enroll right here

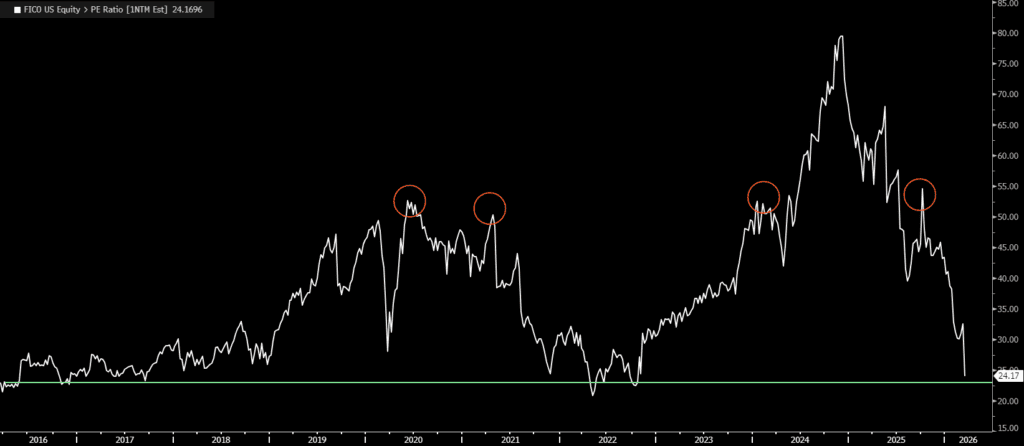

Diving Deeper — Valuation

Trying on the ahead price-to-earnings ratio for FICO reveals an attention-grabbing setup. When the ahead P/E will get above 50, shares are usually overvalued. Nevertheless, now buying and selling at roughly 24 instances earnings, FICO inventory is approaching a 10-year trough. The fear right here is that the inventory will undergo additional valuation compression as a result of dampened sentiment and worries about its aggressive benefit in key markets. Regardless, the valuation has come down considerably whereas key metrics like income and revenue proceed increased.

Dangers

One in all FICO’s key dangers includes rising aggressive and pricing strain in mortgage credit score scores, the place FHFA’s “lender alternative” framework opens the door for loans delivered to Fannie/Freddie to make use of both a Traditional FICO mannequin or VantageScore 4.0, growing the chance of share loss and/or worth concessions. This can be a key enterprise for Truthful Isaac.

AI is one other swing issue: it will possibly strengthen Truthful Isaac’s decisioning software program, however it additionally lowers obstacles for rivals to construct “adequate” underwriting and fraud instruments, doubtlessly compressing differentiation and pricing over time. Even when fundamentals keep strong, investor sentiment might stay depressed if markets view mortgage competitors as structural and AI as accelerating commoditization till FICO proves it will possibly defend pricing and maintain share whereas monetizing AI-led upgrades. Past that, Truthful Isaac faces the identical market-wide, economic-related dangers as many different sectors and industries.

The Backside Line

Truthful Isaac seems to be like a traditional battle between strong fundamentals and weak sentiment — although that sentiment has soured for good cause. Whereas the enterprise continues to be rising, the valuation has reset sharply. That brings each alternative and threat, because the inventory now extra precisely accounts for present dangers, however might be susceptible to additional valuation compression till the corporate exhibits it will possibly navigate mortgage competitors, defend its edge in opposition to AI-driven disruption, and hold development on observe.

Disclaimer:

Please word that as a result of market volatility, among the costs might have already been reached and eventualities performed out.

{kind=link}