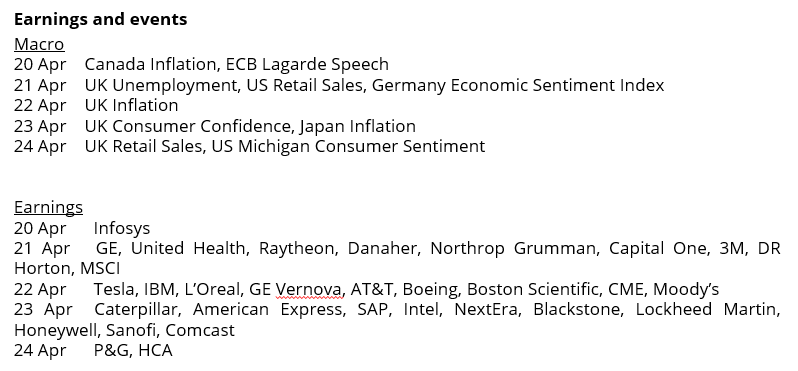

Analyst Weekly, April 20, 2026

Markets received a little bit of aid over the weekend. Experiences that the Strait of Hormuz can be opened despatched oil sharply decrease, with Brent dropping again towards beneath $90. Gasoline costs had already began to ease, and the fast “worst-case” provide shock is off the desk, for now.

But, the system continues to be operating low on buffers, and that retains the stress on discovering a extra sturdy decision within the Center East.

Inventories are the true challenge

Even when flows resume, we’re not ranging from a cushty place.

Latest disruption has already drained inventories

Pre-conflict shipments have largely cleared

Alternative provide has not totally arrived

Monetary markets regulate quick. Sadly, bodily provide doesn’t.

Even in a easy reopening situation:

It takes weeks for manufacturing to ramp

Longer for tankers to normalize

Even longer for inventories to rebuild

Therefore, costs can fall rapidly, however provide tightness can linger.

On the peak of disruption, the worldwide market was successfully quick ~15 to 16 million barrels per day which is a large hole.

If disruptions persist:

Inventories might method operational minimums

Costs would doubtless spike once more

Demand destruction turns into the balancing mechanism

The US is comparatively higher insulated, however Europe and Asia are extra uncovered.

Funding Takeaway: Close to-term dangers have eased, with oil pulling again and development knowledge holding up, which helps a constructive backdrop for threat belongings.Stability in power costs, quite than additional declines, can be wanted to maintain the present growth on observe. Market’s focus now shifts as to if enhancing sentiment is confirmed by knowledge, significantly shopper exercise and companies momentum.

Q1’26 Banks Earnings Name Synthesis: What Issues

We reviewed Q1’26 earnings calls throughout Goldman Sachs, JPMorgan, Citi, Financial institution of America, Morgan Stanley,Wells Fargo, PNC, M&T, and BlackRock.

Stepping again from the noise, the message is pretty clear: the system is holding up higher than sentiment suggests. Exercise stays strong, credit score continues to be clear, and several other key earnings drivers have quietly turned optimistic. That hole between resilient knowledge and cautious expectations is the place the chance sits.

The financial system is softer in surveys than in actuality

Throughout JPMorgan, Financial institution of America, Goldman Sachs, and Wells Fargo, the read-through is constant: purchasers are nonetheless lively.

Spending, borrowing, and deal pipelines aren’t behaving as if a recession is imminent. Financial institution of America framed it greatest; there’s a rising disconnect between weak confidence knowledge and resilient transactional exercise.

Funding Takeaway: This issues as a result of markets are inclined to commerce narratives. Banks function on actual flows. Close to-term draw back threat to earnings from a macro shock nonetheless appears to be like restricted.

Personal credit score: contained, however not irrelevant

There’s a tendency available in the market to border personal credit score as both benign or systemic. The truth sits in between.

Banks are typically snug with their publicity, which is basically senior, structured, and relationship-driven. Nonetheless, they’re extra cautious on the broader ecosystem, the place underwriting requirements are much less constant.

The danger is much less about direct financial institution losses and extra about second-order results: liquidity, sentiment, and refinancing dynamics.

Regulation is shifting from headwind to tailwind

One of many extra underappreciated developments is the evolving regulatory backdrop.

Potential changes to Basel III and capital frameworks are directionally supportive, with implications for:

Decrease capital necessities

Improved returns on fairness

Funding Takeaway: Capital aid might change into a significant medium-term earnings lever, significantly for lower-risk steadiness sheet fashions.

Credit score stays benign however threat is constructing beneath the floor

Present credit score metrics are, by most measures, nonetheless very sturdy:

However administration groups are more and more aligned on the medium-term threat: the subsequent credit score cycle could also be sharper than consensus expects.

The drivers are:

Elevated charges for longer

Pockets of looser underwriting (notably in personal credit score)

Funding Takeaway: Credit score isn’t a present earnings challenge, however it’s the key variable for 2026-2027.

Income high quality is enhancing, however inconsistently

Internet curiosity earnings continues to be supportive, however the drivers have advanced. It’s now extra about asset combine, repricing, and deployment than merely charge path.

The important thing distinction is that not all banks are equally positioned. The corporations with diversified income streams are capturing extra of the upside.

Funding Takeaway: It is a stock-picker’s atmosphere, not a blanket sector commerce.

Mortgage development has inflected

One of many extra necessary shifts this quarter is that mortgage development is now not hypothetical.

Crucially, underwriting requirements stay disciplined.

Funding Takeaway: If mortgage development persists with out margin compression, the sector is getting into a optimistic working leverage part, which helps earnings revisions greater.

Funding takeaways

Want diversified franchises: Banks with publicity to charges, markets, and wealth alongside lending are higher positioned to navigate each resilience and volatility.

Watch mortgage development as the important thing sign: Sustained, broad-based lending development would verify a sturdy earnings upcycle.

Deal with credit score as a lagging threat, not a present downside: Markets could also be early in pricing a downturn that isn’t but seen within the knowledge.

Concentrate on funding high quality, not simply development: Deposit combine and consumer depth will more and more separate winners from laggards.

Don’t ignore capital optionality: Regulatory easing might unlock incremental returns through buybacks and steadiness sheet effectivity.

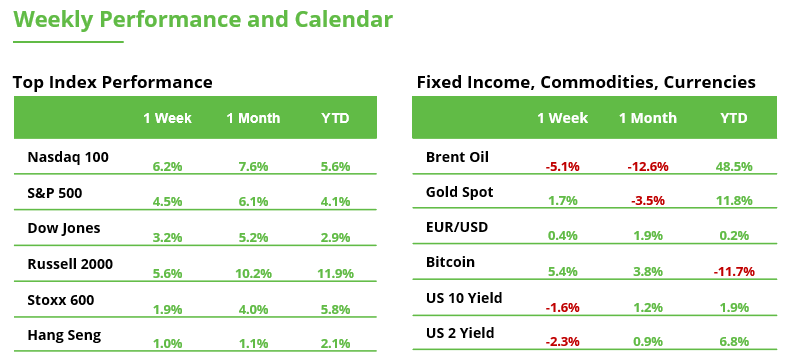

Third consecutive week of positive aspects: Financial institution ETF approaches document excessive

The SPDR S&P Financial institution ETF (KBE) prolonged its restoration final week, marking its third straight week of positive aspects. It rose by one other 2.8% to $65.50. This has diminished the hole to the February document excessive of $67.60 to lower than 5%. The reversal in latest weeks suggests the start of a brand new upward impulse within the broader image, following a stronger corrective transfer.

From a technical standpoint, consideration is now shifting to a possible breakout to the upside, which might verify the long-term uptrend. Prior to now, such breakouts have typically been adopted by strikes of 10% or extra (see blue rectangles), implying upside potential towards the $74 space. Within the occasion of short-term pullbacks, the 20-week transferring common at $61.10 and the March low at $56.80 are more likely to act as key assist ranges.

KBE, weekly chart. Supply: eToro

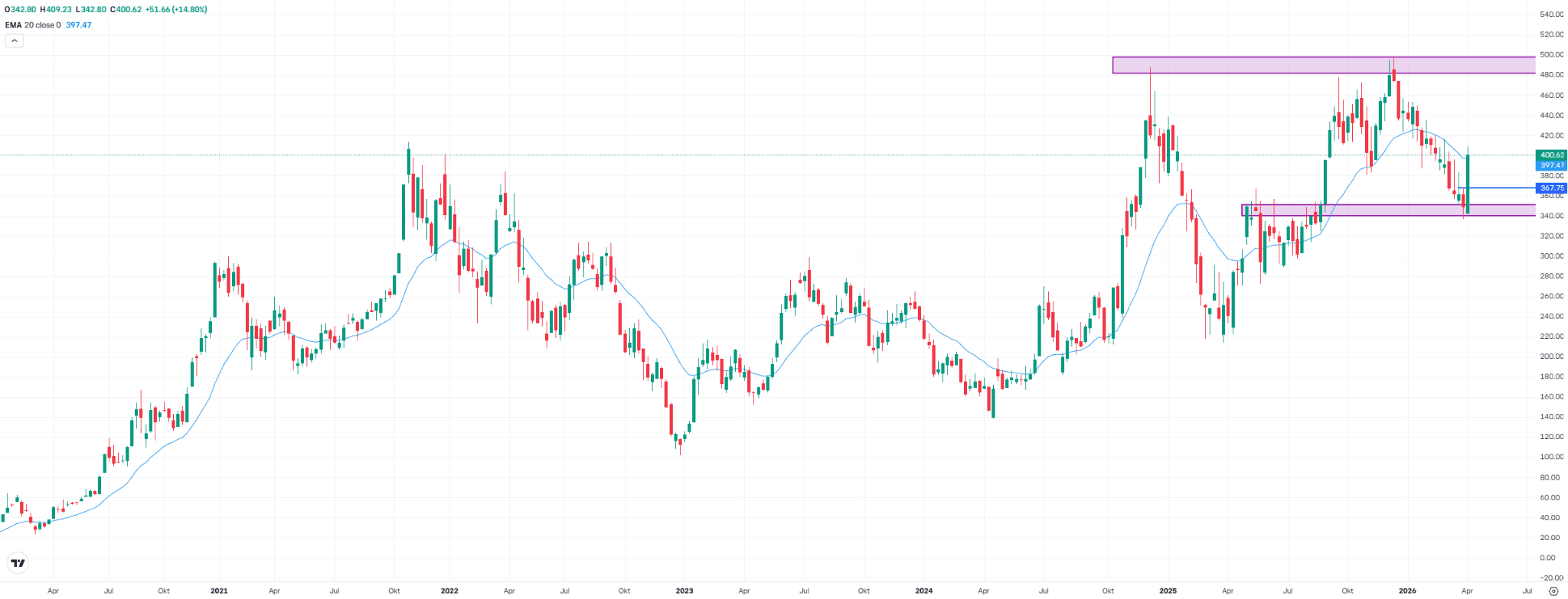

Tesla inventory with a powerful comeback: Is that this the turning level?

Tesla shares rallied sharply final week, gaining 14.8% to shut at $400.60 – the strongest weekly enhance in practically a 12 months. From a technical perspective, that is notable. The previous resistance zone between $340 and $350 (shaped between Might and September 2025) has now acted as assist and served as a springboard for the restoration. As well as, each the excessive from two weeks in the past at $367.80 and the 20-week transferring common at $397.50 have been damaged to the upside.

This factors to a possible turning level within the medium-term development. Whether or not the transfer proves sustainable and the inventory continues towards the December document excessive of $498, or first provides again a few of its latest positive aspects, will largely rely upon the quarterly outcomes due on Wednesday. The outlook can be key, significantly relating to the influence of the Iran battle and persistently excessive oil costs.

Tesla, weekly chart. Supply: eToro

Crypto: Squeeze With out Observe-By means of

The market has begun the transfer, however has not but accomplished it. Friday’s rally responded to mechanical logic quite than a structural shift: excessive quick positioning, an exterior catalyst, and a technical breakout that compelled large liquidations. Almost $600M in shorts have been eradicated, however the system was not left clear.

Since then, value has misplaced continuity. Not from an absence of demand, however as a result of the atmosphere has reasserted itself. Geopolitics has reintroduced a binary element that displaces any market-driven narrative. On this regime, belongings don’t anticipate: they react.

Even so, there are indicators price not ignoring. Institutional move has been decisive at these moments, as proven by ETFs that recorded near $1B in weekly inflows. This stage of absorption validates that actual demand exists on dips and through stress occasions. Nonetheless, it’s not but constant or aggressive sufficient to maintain a breakout.

In parallel, inner tensions are showing. Within the $76,500–$76,800 zone, on-chain knowledge displays distribution by long-term holders. The rise in change deposits means that a part of the market is utilizing the liquidity generated by the squeeze to unwind positions at break-even. It’s, in essence, a market in unstable equilibrium: institutional demand absorbs, however structural provide limits.

Positioning stays the important thing ingredient. The imbalance that triggered the transfer has not disappeared. Shorts persist that would gasoline a second leg if the context cooperates. However that “if” now not relies upon in the marketplace.

Ethereum, in the meantime, is starting to trace at relative power. It isn’t but a regime change, however it’s an early sign. The narrative, tokenization, settlement infrastructure, stays intact, even when the worth doesn’t replicate it. Its alternative stays a long-horizon one, not short-term.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private advice, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out taking into consideration any specific recipient’s funding targets or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product aren’t, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}