A brand new international monetary disaster is just not confirmed, however the path towards one is now seen sufficient to map.

The sequence begins with debt and oil earlier than it reaches credit score. Lengthy-end sovereign yields and Brent crude are already shut sufficient to emphasize ranges to make the coverage squeeze pressing.

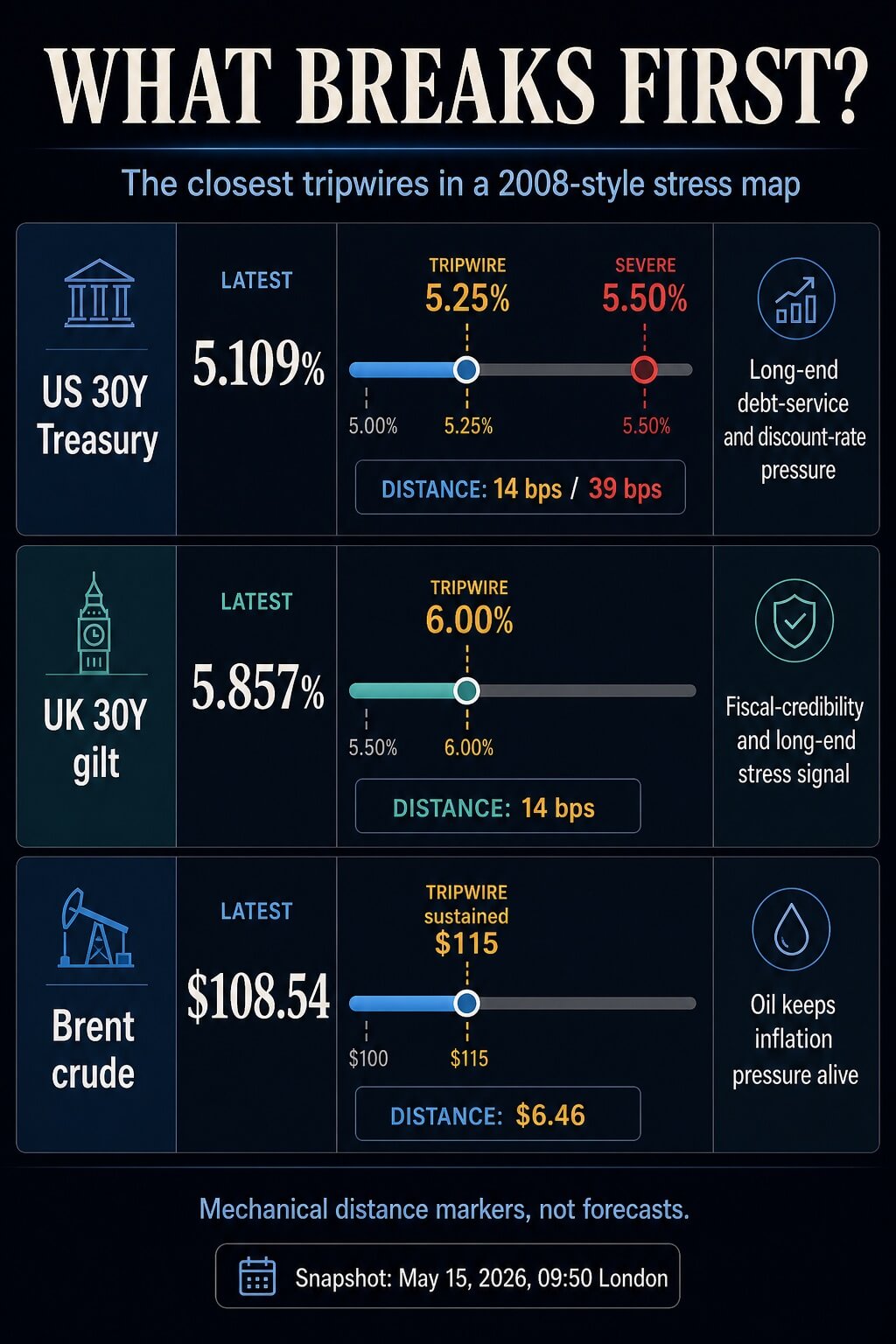

To shut out the week, the US 30-year Treasury yield was close to 5.109%, the UK 30-year gilt was close to 5.857%, Brent was close to $108.54, and the VIX was close to 18.53.

These numbers level to a market shifting towards the a part of the map the place a bond shock and an oil shock can begin forcing different markets to reply.

The excellence is sensible. A 30-year Treasury yield above 5.25%, a UK 30-year gilt above 6%, or sustained Brent above $115 would all worsen the debt-service and inflation drawback.

However a 2008-style occasion wants greater than costly authorities debt and power. It wants stress emigrate into credit score, volatility, monetary circumstances, funding markets, and compelled promoting.

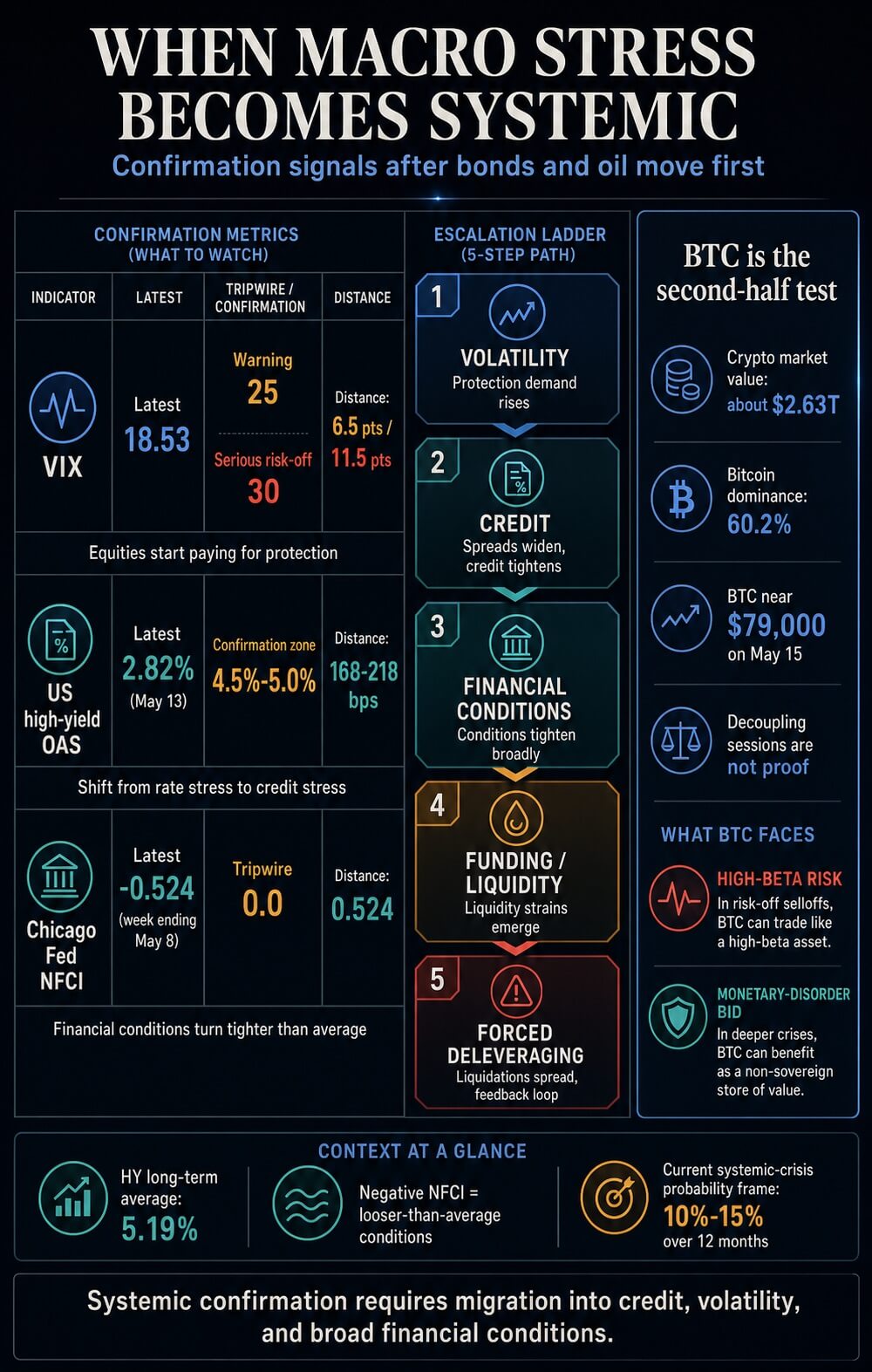

The broad information nonetheless reveals a distinct image. US high-yield option-adjusted spreads have been nonetheless solely 2.82% on Could 13, beneath the long-term common of 5.19%.

A later FRED replace put the identical credit-spread household at 2.76% for Could 14. The Chicago Fed Nationwide Monetary Circumstances Index was nonetheless -0.524 for the week ending Could 8, and destructive NFCI readings point out looser-than-average monetary circumstances.

That leaves markets in a break up state: the warning indicators are shut, however the affirmation indicators haven’t arrived.

The dashboard markets ought to watch

IndicatorLatest readingTripwireDistanceWhat it means if brokenUS 30Y Treasury5.109percent5.25% warning, 5.50% extreme stressAbout 14 bps to five.25%, 39 bps to five.50percentLong-end debt-service strain begins trying like a fiscal and discount-rate drawback, not only a bond-market transfer.UK 30Y gilt5.857percent6.00percentAbout 14 bpsUK long-end stress strikes right into a fiscal-credibility zone that may spill into sterling, pensions, and danger belongings.Brent crude$108.54Sustained $115About $6.46Oil retains inflation strain alive and limits the power of central banks to rescue markets shortly.VIX18.5325 warning, 30 severe risk-offAbout 6.5 factors to 25, 11.5 factors to 30Equity markets cease treating the shock as background noise and begin paying for cover.US high-yield OAS2.82% on Could 134.5%-5.0percentAbout 168 bps to 4.5%, 218 bps to five.0percentThe story shifts from fee stress into credit-event affirmation.Chicago Fed NFCI-0.524 for week ending Could 80.00.524 index pointsBroad monetary circumstances cross into tighter-than-average territory.

The closest breaks are the US 30-year, the UK 30-year, and Brent. The extra necessary affirmation factors are high-yield spreads, VIX, and NFCI.

A mechanical one-day gauge reveals why the primary group issues. If the US 30-year repeated its 9.6 basis-point each day transfer, it could attain 5.25% in roughly 1.5 buying and selling days and 5.50% in roughly 4.

If the UK 30-year repeated its 20.6 basis-point transfer, 6% could be lower than one buying and selling day away. If Brent repeated its $2.82 each day achieve, $115 could be two to 3 buying and selling days away.

Deal with these as distance markers, not forecasts. They present how shut the market is to ranges the place the narrative modifications.

Why bonds and oil break first

Lengthy-end yields are the primary strain level as a result of they transmit stress into nearly all the things else.

For governments, greater 30-year yields increase the price of refinancing on the identical time budgets are already beneath strain. The IMF’s April 2026 Fiscal Monitor mentioned international public debt rose to simply beneath 94% of GDP in 2025 and is projected to achieve 100% by 2029, with public funds strained by rising curiosity burdens.

That makes each long-end yield spike greater than a chart occasion. It raises the value of time for governments, households, banks, insurers, pensions, and corporations that depend on long-duration valuations.

The transmission can arrive with out a single dramatic failure. Increased long-end charges can decrease the worth of bond portfolios, strain mortgage and company refinancing prices, and make fairness valuations more durable to defend.

In addition they pressure governments to decide on between tighter budgets, heavier issuance, and better curiosity payments. A transfer from stress to disaster can begin quietly in period markets earlier than it reveals up in layoffs, financial institution funding, or default danger.

Oil provides the second strain channel. The EIA described the Strait of Hormuz as a essential chokepoint, with 2024 oil flows averaging about 20 million barrels per day, or roughly 20% of worldwide petroleum liquids consumption.

The World Financial institution mentioned Brent may common as excessive as $115 in 2026 beneath a severe-disruption state of affairs involving harm to essential oil and gasoline services and gradual export restoration.

Brent is central to the GFC query as a result of it could possibly hold inflation elevated, weaken actual incomes, strain margins, and cut back the room central banks have to chop charges if markets begin to fall.

It doesn’t must straight break the banking system to make a subsequent credit score occasion more durable to battle.

In 2008 and 2020, policymakers may ultimately transfer exhausting towards monetary rescue. On this setup, the constraint is completely different.

Rescue too early, and inflation credibility comes beneath strain. Wait too lengthy, and monetary stability can break first.

What would affirm the shift into systemic stress

The exhausting break requires greater than the US 30-year alone. A 5.25% or 5.50% 30-year Treasury could be a serious warning, however it could nonetheless be a warning.

The identical holds for a 6% UK 30-year gilt or Brent above $115.

The affirmation would come from migration.

First, volatility would wish to cease trying orderly. A VIX transfer via 25 would present fairness traders paying up for cover.

A transfer via 30 could be a extra severe risk-off sign, particularly if it got here whereas lengthy yields and oil have been nonetheless rising.

Second, credit score would wish to reprice. The high-yield unfold, round 4.5% to five.0%, is the extra necessary line as a result of it could point out that traders are now not treating the shock as a fee drawback.

They might demand extra compensation for default and liquidity danger.

That’s the level at which the story shifts from macro strain to credit score stress. The gap from 2.82% to 4.5% is about 168 foundation factors.

That hole is why the present proof falls wanting a 2008-style credit score occasion.

Third, monetary circumstances would wish to tighten broadly. An NFCI crossing above zero would point out that the stress is now not confined to charges, oil, or equities.

It will imply cash markets, debt markets, fairness markets, and the banking system are collectively tighter than common.

Solely after that will the actual systemic channel come into sight: funding strain, collateral calls, liquidity holes, financial institution balance-sheet stress, and compelled deleveraging.

That’s the half that turns a harsh macro correction right into a monetary disaster.

On present proof, that is still a second-order state of affairs. An affordable 12-month vary stays round 10% to fifteen%, rising towards 15% to twenty% if the US 30-year breaks 5.25%, the UK 30-year breaks 6%, Brent stays above $115, and the VIX strikes above 25.

A high-yield unfold transfer via 4.5% would matter greater than any single bond print as a result of it could present credit score catching the shock.

The place Bitcoin suits into the check

Bitcoin comes after the macro check.

The crypto market is massive sufficient to react to the identical liquidity forces driving shares, bonds, and commodities. CryptoSlate’s market pages present a complete crypto market worth of $2.6 trillion, with Bitcoin dominance round 60%.

The Bitcoin web page reveals BTC close to $78,000 going into the weekend, down about 2.8% over 24 hours.

Latest CryptoSlate protection has already proven why the Bitcoin sign is difficult. BTC has at occasions damaged from US equities whereas oil, yields, and the greenback pressured shares, with Bitcoin now beneath $80,000 even because the S&P 500 hits new information.

Nonetheless, one or two decoupling periods fall wanting proving a sturdy regime change. If this stays a bond-and-oil shock with out credit score affirmation, Bitcoin could commerce the standard mixture of liquidity expectations, real-rate strain, greenback strikes, ETF flows, and danger urge for food.

It will possibly diverge for a session or two with out proving that it has turn out to be a disaster hedge.

If the shock strikes additional into credit score, the check turns into more durable. In a real deleveraging section, traders promote what they will, not solely what they wish to promote.

Bitcoin may commerce like high-beta collateral first, particularly if volatility rises and liquidity turns into scarce.

The bullish macro case would wish to outlive that section. BTC must present investor demand, treating it as safety towards fiscal stress, financial dysfunction, or coverage credibility danger after the forced-selling strain subsides.

That may be a greater bar than outperforming shares on a blended macro day.

The trail additionally depends upon what drives the selloff. A rates-led repricing tends to strain long-duration belongings and speculative publicity.

An oil-led inflation shock can hit danger urge for food whereas additionally elevating questions in regards to the buying energy of fiat. A credit-led break is harsher as a result of it turns liquidity right into a scarce asset.

Bitcoin’s response throughout these three states would inform markets greater than any single each day correlation print.

The road between correction and disaster

Markets are nonetheless wanting saying 2008 is right here. But they are saying the trail to that form of occasion is seen sufficient to watch in actual time.

The primary a part of the trail is already shut: long-end US and UK yields, oil, inflation strain, and constrained central banks.

The second half continues to be lacking: high-yield spreads above 4.5% to five.0%, VIX above 25 to 30, and NFCI above zero.

That distinction signifies that if a brand new GFC-style occasion is growing, the bond and oil numbers ought to break first.

The affirmation comes solely when credit score, volatility, and monetary circumstances observe.

Till then, the label is a harmful macro-correction danger moderately than a confirmed systemic disaster.

{kind=link}