{kind=link}

For our newest installment of Finovate First-Timers, a brand new collection profiling firms that just lately made their debuts on the Finovate stage, we meet up with Marco Ma, Co-Founder and CEO of Ventus AI. Ventus AI helps banks personalize each touchpoint throughout the shopper journey, boosting engagement, lifetime worth, and belongings underneath administration.

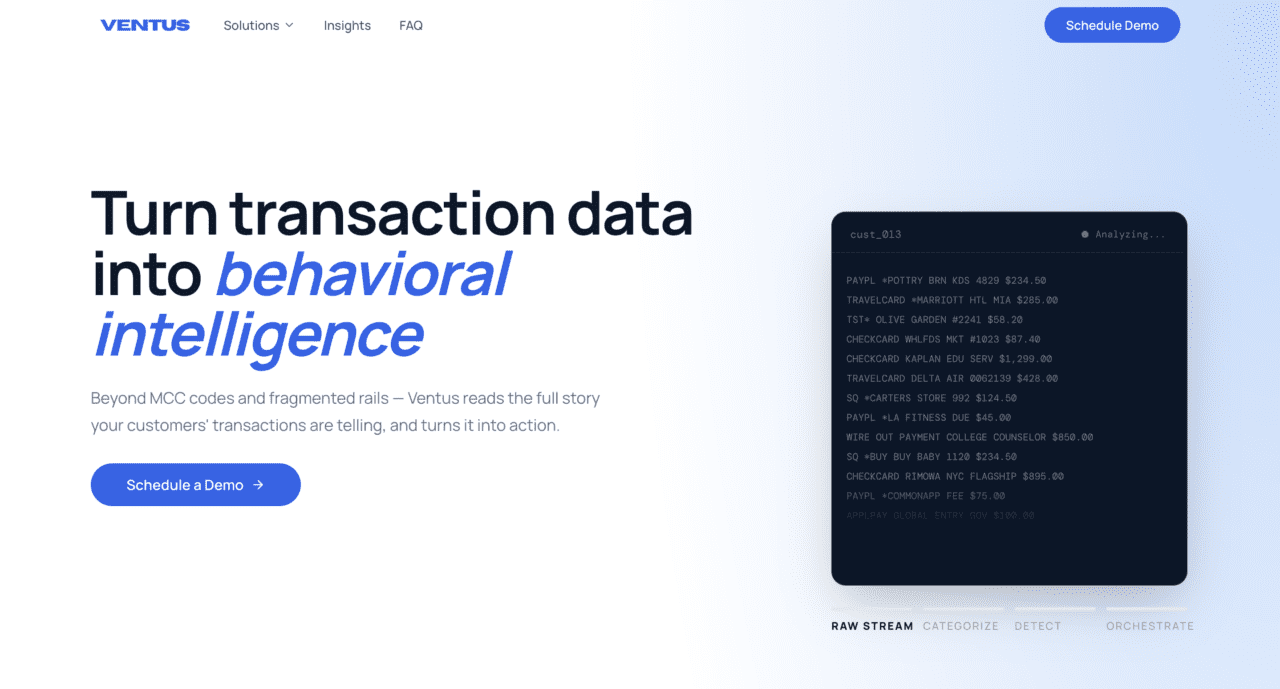

The corporate’s know-how transforms uncooked transaction knowledge right into a cross-categorized behavioral intelligence layer that spans greater than 3,000 spending subcategories to floor life occasions, dynamic personas, and real-time intent indicators. Based in 2025 and headquartered in New York, Ventus AI demoed its know-how at FinovateSpring 2026 in San Diego, California.

On this week’s dialog, Ma talks in regards to the challenges banks and credit score unions face in terms of leveraging knowledge to create higher, extra personalised experiences for purchasers and members. He explains how Ventus AI plugs into present stacks to offer a brand new analytics layer that delivers solutions to questions on buyer preferences and ache factors with out constructing something new.

What drawback does Ventus AI resolve and who does it resolve it for?

Marco Ma: Banks sit on monumental volumes of transaction knowledge, however most of it stays trapped as uncooked, messy information their groups can’t truly learn. The result’s a lose-lose: prospects get served demoralizing generic experiences which ends up in misplaced relationships and deteriorated buyer economics. We resolve this for banks and credit score unions that wish to perceive and serve their prospects extra deeply.

How does Ventus AI resolve this drawback higher than different firms?

Ma: We constructed a proprietary buyer intelligence and personalization engine. It really works throughout each account and cost rail and detects the complete image: way of life patterns, life-event triggers, monetary vulnerability indicators, and semantic budgeting. The place most instruments cease at cleansing up a service provider identify, we floor what’s truly taking place in a buyer’s life, and we ship it into the instruments banks already use relatively than asking them to tear something out.

Who’re Ventus AI’s main prospects, and the way do you attain them?

Ma: US monetary establishments, with our preliminary concentrate on banks and credit score unions within the $1 billion to $50 billion asset vary, alongside an lively enterprise pipeline. We attain them by means of business applications and conferences like Finovate and the Fintech Sandbox community, direct relationships constructed by the founding group, and heat introductions by means of our advisors and ecosystem companions.

Are you able to inform us a few favourite implementation or partnership expertise?

Ma: Our favourite work is on rewards and offers. The perception that makes it particular is that the identical supply can imply utterly various things to totally different individuals. Folks don’t get up someday and say “I wish to store at Crate & Barrel.” Some individuals desire a new espresso machine, some individuals desire a new facet desk. As a result of we perceive the habits behind the spend, the financial institution can current the identical deal in the best way that really resonates with every individual, turning a generic coupon e-book expertise into one thing that feels private.

What in your background gave you the arrogance to reply to this problem?

Ma: Now we have a powerful founding group with backgrounds spanning Visa, McKinsey, AWS, and Credit score Suisse, together with distinguished advisors from the banking world. That blend of funds, knowledge, and institutional banking expertise meant we understood each the technical drawback and the best way banks truly purchase and undertake know-how.

You demoed at FinovateSpring in Could. How was the expertise?

Ma: It was an amazing second for us. Banking is deeply private. It touches crucial moments in individuals’s lives, and our hero demo follows an expecting-parent spending sample throughout rails to point out we are able to extract main life occasion indicators and orchestrate the present tech stack—rewards, product, relationship—to be personalised to assist this buyer by means of this journey. Demoing that dwell on the principle stage reminded us why this issues: accomplished proper, this know-how lets a financial institution present up for somebody at precisely the second it counts. We’re returning for the Fall present.

You have been accepted into the Fintech Sandbox Knowledge Entry Residency. What’s it, and why does it matter?

Ma: Fintech Sandbox provides early-stage fintech firms entry to high-quality monetary knowledge and infrastructure to construct and refine their merchandise. For us, it’s significant as a result of behavioral intelligence is just pretty much as good as the info it learns from. The residency accelerates our potential to develop and validate our engine towards actual, wealthy datasets, which straight strengthens what we ship to banks.

What are your targets for the remainder of 2026 and into subsequent yr?

Ma: Develop our pipeline by means of enterprise growth, transfer lively conversations into dwell deployments, return to the Finovate predominant stage within the Fall, and shut our present funding spherical. Past that, we’re heads-down constructing, deepening the behavioral sign we ship and increasing what banks can do with it.

Picture by Suzanne D. Williams on Unsplash

Views: 5