The stablecoin market has lengthy rewarded the businesses that concern digital {dollars}. They absorb buyer money, maintain reserves in short-term authorities securities, and earn the yield.

Now, the businesses that distribute these tokens need extra of the economics.

That pressure is on the middle of Open USD (OUSD), a deliberate stablecoin backed by greater than 140 monetary, expertise, and crypto companies, together with Coinbase, Visa, Mastercard, Stripe, BlackRock, and Google.

The venture guarantees free minting and redemption for companies, in addition to a reserve-income mannequin that sends extra worth to the platforms driving adoption.

For Circle, the USD Coin (USDC) stablecoin issuer, an important title on that record is Coinbase.

The trade helped flip USDC into one among crypto’s most generally used greenback tokens. Coinbase mentioned in its first-quarter report that greater than 25% of USDC in circulation, or about $19 billion on common, was held throughout its merchandise. It additionally mentioned Base, its layer-2 community, processed 62% of world on-chain stablecoin transaction quantity through the quarter.

That makes Coinbase’s assist for OUSD greater than a symbolic endorsement. It offers Circle’s most vital distribution associate a stake in a rival mannequin simply because the economics of stablecoin issuance have gotten extra contested.

The price of distribution

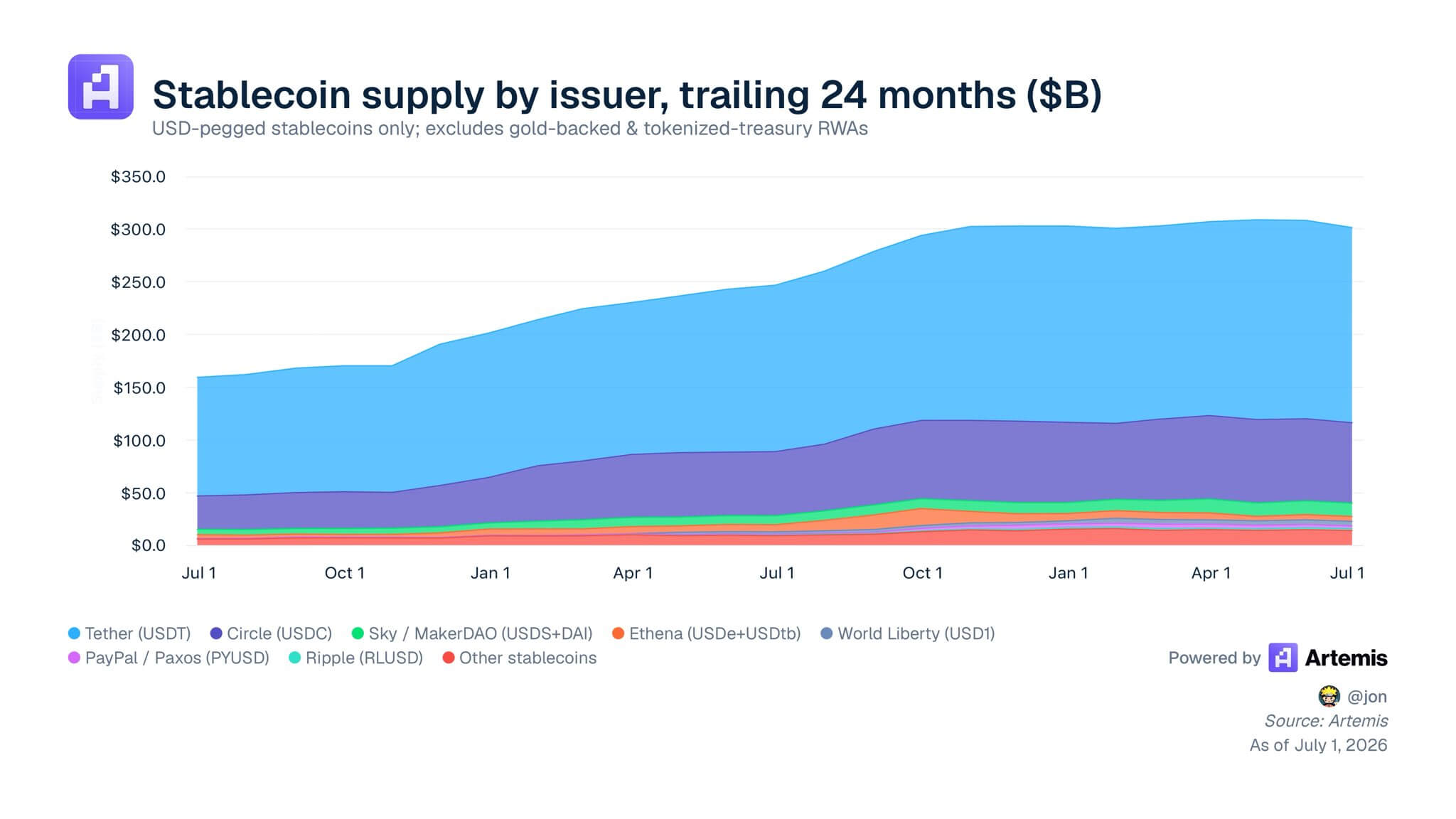

OUSD’s consortium launch represents a direct problem to the incumbent stablecoin sector, which at present instructions a market capitalization exceeding $320 billion.

For years, pure-play issuers like Circle and Tether have operated high-margin fashions by retaining the curiosity earnings generated from the billions of {dollars} backing their tokens.

Nevertheless, as stablecoins migrate from speculative buying and selling property to foundational rails for international settlement and funds, the businesses offering the precise buyer pipelines are demanding a basic realignment of the revenue-sharing structure.

OUSD addresses this by aiming to remove normal minting or redemption charges and to structurally return a lot of the reserve yield on to its distribution companions.

The fast market affect was palpable, with Circle’s shares falling 16% on the day the consortium was introduced. The drop underscores investor anxiousness concerning the sturdiness of Circle’s core business relationship with Coinbase.

That relationship has traditionally been extremely profitable however more and more advanced. In 2024, Circle paid Coinbase $908 million underneath their revenue-sharing settlement, reflecting the trade’s position as one among USDC’s most vital distribution and liquidity channels.

Public monetary disclosures present that Coinbase captured a bigger share of the USDC income pool than many traders anticipated, highlighting the premium positioned on distribution over uncooked issuance.

For the complete 12 months 2025, Coinbase’s stablecoin-tied income totaled roughly $1.35 billion, accounting for roughly 19% of its complete annual income.

So, Coinbase’s pivot towards a founding position in OUSD offers it a strong different asset precisely when its present contract with Circle approaches a important milestone. The distribution settlement between the 2 companies operates on a three-year cycle, with the following expiration date set for August 2026.

Tiger Analysis acknowledged that stepping to the negotiating desk as a central architect of a competing, distributor-first stablecoin gives Coinbase with substantial business leverage.

Coinbase CEO Brian Armstrong saved public feedback temporary, stating solely that the agency is “excited to advance the adoption of stablecoins” and replace the worldwide monetary system.

Nevertheless, the underlying mechanics counsel a broader trade realization: the entities that management the distribution community are not keen to depart the majority of reserve curiosity earnings on the desk.

Circle Defends the Incumbent Mannequin

Circle is pushing again in opposition to the narrative that distribution can simply replicate built-in community infrastructure.

In an X publish, Circle CEO Jeremy Allaire mounted an in depth protection of the USDC community, arguing that stablecoins function as platform and network-effect companies that have a tendency towards “winner-take-most” buildings over prolonged horizons.

Allaire, citing Artemis knowledge, acknowledged that USDC dealt with practically $30 trillion in on-chain transaction quantity through the first quarter of 2026, accounting for 80% of all dollar-denominated stablecoin transactions throughout main blockchains.

He famous:

At this time, USDC is within the high 3 most liquid digital property on the earth, and it falls off sharply after that. BTC, USDT and USDC have extraordinary liquidity. The closest different greenback stables are like 10x smaller and that liquidity tends to be concentrated in promotional books in a single trade, whereas USDC liquidity is dispersed extensively throughout dozens and dozens of surfaces. Constructing this liquidity has been a virtually decade-long job that we proceed.

Allaire maintained that these metrics mirror practically a decade of deep integration that can’t be immediately substituted by a company coalition. He emphasised that USDC’s presence throughout main monetary market facilities, decentralized finance (DeFi) protocols, and international fee service suppliers creates an operational moat.

Addressing OUSD’s price construction, Allaire famous that whereas zero-fee fashions sound interesting in advertising supplies, market realities typically require extra structured business approaches.

He indicated that Circle already mitigates transaction friction by means of bespoke contractual agreements with its enterprise fee companions somewhat than counting on blanket price exemptions.

Moreover, Allaire questioned the operational viability of large-scale company alliances within the fast-moving digital asset house, describing the historic efficiency of economic consortia as “predictably slow-moving.”

He remarked:

“Massive teams of huge corporations coordinate poorly, have misaligned incentives, gradual issues down and barely create the house for actual sturdy innovation and competitiveness.”

He revealed that Circle experimented with a restricted consortium construction throughout USDC’s early years however discovered that smaller, autonomous strategic collaborations constantly outpaced committee-driven networks.

From an operational standpoint, Allaire warned that gifting away all reserve earnings leaves a stablecoin community with out the retained capital wanted to fund international licensing, compliance, and 24/7 treasury administration infrastructure.

OUSD faces obstacles to scale

Market analysts additionally categorical warning concerning how successfully OUSD can translate its spectacular record of company logos into lively on-chain liquidity.

Lorenzo Valente, Director of Analysis for Digital Belongings at ARK Make investments, famous that any new stablecoin faces a extreme “cold-start” dilemma. Capital markets and crypto exchanges are closely optimized round entrenched buying and selling pairs denominated in USDT and USDC.

He wrote:

“A consortium of 500 rivals has no precedent for working. Circle and Tether ship no matter they need, every time they need, with zero dedication to anybody. The tempo of decision-making throughout rivals goes to be glacial.”

Valente additionally raised considerations about regulatory and antitrust scrutiny. Whereas Circle and Tether have spent years accumulating a number of licenses and regulatory relationships worldwide to face up to international regulatory stress, a unified issuance car backed concurrently by the world’s largest bank card networks, asset managers, and retail banks represents a high-profile goal for antitrust regulators.

In the meantime, the long-term alignment of OUSD’s founding members stays a variable.

Stripe not too long ago acquired the stablecoin infrastructure agency Bridge and continues to develop its unbiased fintech suite. Main banking companions are testing proprietary tokenized deposit programs, whereas companies like Ripple are rolling out their very own specialised stablecoins.

As a result of these large distribution networks are actively hedging their methods throughout a number of concurrent digital asset merchandise, the shortage of unique distribution commitments may dilute OUSD’s community velocity.

In view of this, Kayla Phillips, the blockchain VC at Hivemind, mentioned:

“How will all these events coordinate and govern? Appears unlikely that each one 140 can have an equal seat on the desk, if they need this to be efficient. If not on the governing board, will they nonetheless be incentivized to take part within the consortium?”

The fragmentation of on-chain settlement

The emergence of OUSD highlights a broader development towards the fragmentation and potential abstraction of the stablecoin layer.

Somewhat than working as a standalone consumer-facing product, the expertise is more and more considered by main firms as a commoditized back-end settlement mechanism.

For Circle, sustaining its market share would require accelerating the deployment of its value-added developer stacks, equivalent to its Cross-Chain Switch Protocol (CCTP) and embedded institutional wallets, making certain that its software program layer gives utility that goes past primary curiosity margin distribution.

Finally, the competitors over stablecoin supremacy has shifted from technical implementation to a direct negotiation over community economics.

As distribution platforms set up to retain extra of the yield generated by their very own person bases, the issuer-led mannequin faces its strongest distribution-side problem but.

{kind=link}