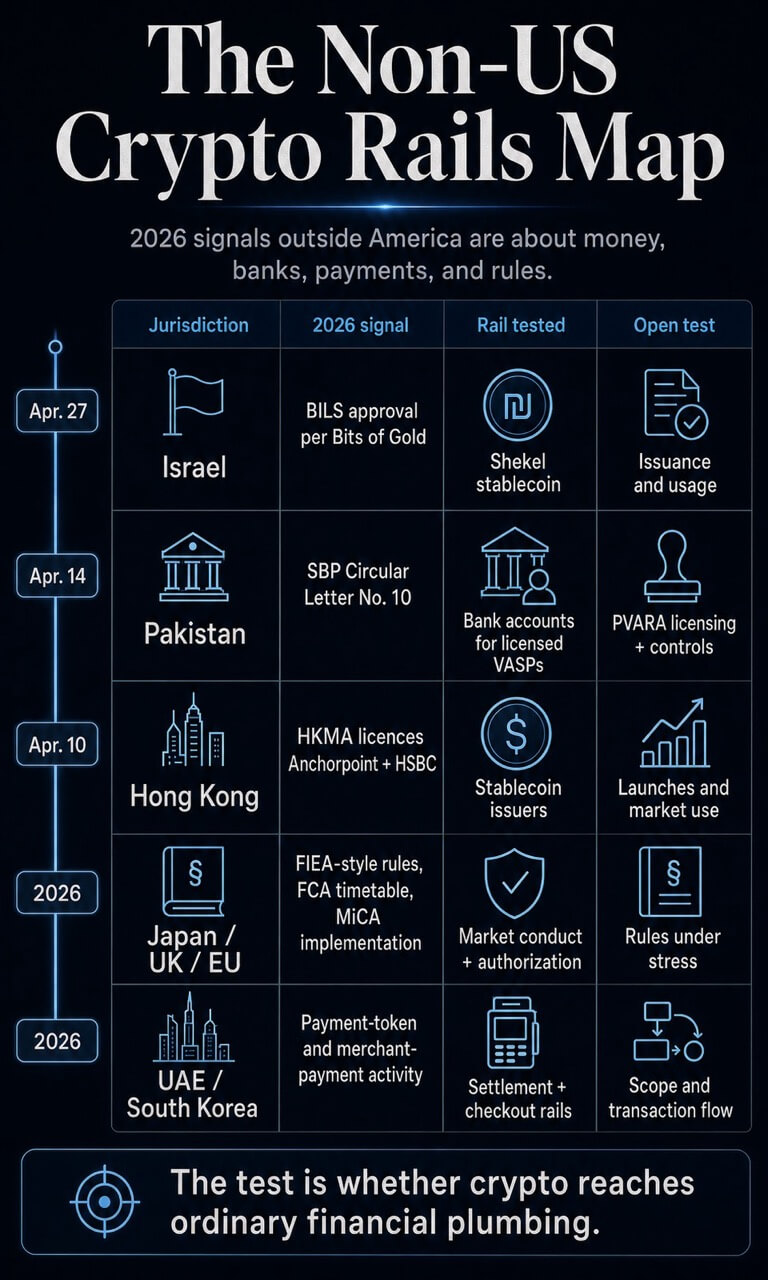

This month, Israel and Pakistan equipped a quieter check for crypto than the one enjoying out in US capital markets. What if the extra necessary 2026 shift is going on the place digital property meet native cash and financial institution accounts?

Israeli crypto agency Bits of Gold mentioned Israel’s Capital Market Authority authorized the issuance and distribution of BILS, a shekel-pegged stablecoin, after a two-year pilot. Days earlier, the State Financial institution of Pakistan issued BPRD Round Letter No. 10 of 2026, changing its 2018 virtual-currency prohibition.

The Pakistan round permits regulated entities to open financial institution accounts for PVARA NOC or licensed VASPs and their prospects below outlined compliance circumstances.

These two strikes sit removed from the US spot ETF cycle. But they level to the operational layer that decides whether or not crypto turns into greater than an funding wrapper. The US has equipped legitimacy, liquidity, and a strong digital-dollar debate.

Different jurisdictions are testing a special working layer: whether or not crypto can hook up with native cash, financial institution accounts, service provider checkout, and enforceable market guidelines.

That distinction adjustments how international adoption must be evaluated. A Bitcoin ETF lets buyers purchase publicity. A regulated shekel stablecoin lets customers maintain a home forex on-chain.

A central financial institution round that lets licensed crypto corporations open accounts offers the sector a bridge again into supervised banking. The primary validates an asset class. The second and third check whether or not crypto can change into usable monetary infrastructure.

The check stays early. BILS nonetheless wants proof of issuance and utilization. Pakistan nonetheless wants licensed VASPs with precise financial institution relationships. Hong Kong’s new licensees nonetheless want enterprise launches.

The UAE nonetheless wants clearer public mapping between dirham-token bulletins and Central Financial institution register entries. Nonetheless, the sample is changing into more durable to dismiss: in 2026, the sensible crypto work is more and more about the place digital property contact cash, banks, retailers, and settlement techniques.

Native cash and financial institution entry

Bits of Gold says the authorized BILS undertaking is a shekel-pegged stablecoin designed initially on Solana, with Fireblocks, QEDIT, EY, and the Solana Basis concerned within the pilot.

The coverage sign is the local-currency part. BILS brings the shekel into an on-chain market nonetheless dominated by greenback stablecoins and asks whether or not a nationwide forex can acquire a programmable model with out ceding your entire funds layer to USD tokens.

That’s the monetary-sovereignty angle. Greenback stablecoins have change into the working unit of a lot of crypto’s settlement exercise.

A shekel token, if issuance and adoption observe approval, offers Israel a approach to check domestic-currency rails inside that very same infrastructure. The end result can be measured much less by market consideration and extra by whether or not wallets, exchanges, fee corporations, and controlled counterparties discover a cause to make use of it.

Pakistan provides the banking half of the opening. The State Financial institution of Pakistan round is concrete as a result of it replaces FE Round No. 3 of 2018 and permits SBP-regulated entities to open accounts for PVARA NOC or licensed VASPs and their prospects.

The round additionally ties entry to financial institution controls, documentation, monitoring, customer-risk checks, and compliance with Pakistan’s virtual-asset framework.

That adjustments the working floor for licensed crypto corporations. Financial institution accounts are fundamental monetary plumbing. They decide whether or not a regulated VASP can maintain shopper cash, reconcile flows, fulfill due diligence, and produce exercise into monitored channels.

For a market equivalent to Pakistan, which Chainalysis ranks amongst main crypto adoption international locations, banking entry can determine whether or not utilization stays casual or strikes into traceable institutional constructions.

Hong Kong affords a licensing comparator for a similar rails-first sample. On April 10, the Hong Kong Financial Authority granted stablecoin issuer licenses to Anchorpoint Monetary Restricted and The Hongkong and Shanghai Banking Company Restricted.

The HKMA register lists each with efficient dates of April 10, 2026. That strikes the jurisdiction from coverage design to named licensed issuers, whereas leaving the business-launch and user-adoption checks forward.

The early map is simple:

Jurisdiction2026 signalRail being testedOpen testIsraelBits of Gold approval statementLocal-currency stablecoinIssuance, redemption, and consumer uptakePakistanSBP Round Letter No. 10Bank accounts for licensed VASPsPVARA licensing and financial institution controlsHong KongHKMA stablecoin issuer licensesNamed licensed issuersLaunches and market useJapan, UK, EURulemaking and implementation clocksMarket conduct and authorizationHow guidelines behave below stressUAE, South KoreaPayment-token and merchant-payment activitySettlement and checkout railsScope, transaction stream, and adoption

Rulebooks have gotten working layers

The identical motion exhibits up in conduct guidelines. Japan’s Monetary Providers Company has revealed supplies pointing towards a shift from Fee Providers Act therapy to Monetary Devices and Alternate Act-style oversight for crypto-assets.

The working-group report recommends info provision, crypto-asset service-provider controls, market-abuse guidelines, insider-trading guidelines, SESC powers, and stronger consumer safety. The FSA’s weekly evaluate additionally notes draft Acts submitted to the Weight loss program tied to FIEA and PSA amendments.

Japan’s sign is about classification and conduct. Crypto property are being pulled towards a framework the place disclosure, surveillance, and misconduct guidelines form participation. That makes entry conditional on habits, supervision, and accountability.

It additionally exhibits why regulatory design generally is a type of infrastructure. Markets use regulation as a routing layer when individuals must know who can record property, who can custody them, who can market them, and which types of buying and selling habits create legal responsibility.

The UK is constructing an identical working layer with an extended runway. The FCA says corporations that need to keep on new regulated cryptoasset actions can apply from Sept. 30, 2026 to Feb. 28, 2027.

The brand new regime is predicted to come back into pressure on Oct. 25, 2027. A associated session discover exhibits the regulator shifting via authorization, supervision, consumer-duty, custody, prudential, and market-abuse work.

Europe already has the broader framework in place. ESMA says MiCA establishes uniform guidelines for crypto-assets masking transparency, disclosure, authorization, supervision, client info, market integrity, and monetary stability.

A broader international regulatory map has already proven regulation shifting as a multi-market course of. The 2026 layer provides a sharper level: rulebooks are beginning to determine how crypto merchandise enter unusual monetary channels.

The UAE provides a payment-token instance, however scope stays the constraint. The Central Financial institution’s Fee Token Providers Regulation gives the rulebook for payment-token exercise, whereas a February CBUAE register gives a public examine on licensed entities.

Individually, an ADX-hosted launch says IHC, Sirius, and FAB obtained CBUAE approval to launch the dirham-backed DDSC on ADI Chain for institutional funds, settlement, treasury, and commerce flows.

For now, the proof factors to a regulated payment-token framework and institutional settlement ambition; broad retail utilization would want separate proof.

South Korea provides a service provider layer. Crypto.com and KG Inicis mentioned in March that they might combine Crypto.com Pay throughout KG Inicis’s service provider community for overseas vacationers and Okay-commerce customers, with retailers capable of obtain fiat or digital property.

South Korea’s Okay Financial institution partnership with Ripple factors to a different rail the place financial institution and funds exercise intersects with crypto. Each examples nonetheless want transaction knowledge.

Their relevance is that they transfer the adoption debate towards checkout, settlement, remittance, and consumer-facing entry.

Utilization is the more durable check

The US-centered interpretation stays highly effective as a result of the numbers are giant. On April 29, whole crypto market capitalization stood close to $2.59 trillion, with Bitcoin round $1.56 trillion.

Greenback stablecoins nonetheless dominate the working liquidity layer, with Tether‘s 24-hour quantity close to $111.50 billion and USDC close to $47.84 billion.

These figures clarify why US coverage and greenback rails preserve pulling consideration. The greenback stablecoin system is already giant. US capital markets provide legitimacy at scale.

The CLARITY Act stablecoin battle exhibits that the US debate can also be about who captures the economics of digital {dollars}. That benchmark stays important, as a result of international crypto infrastructure nonetheless relies upon closely on greenback liquidity.

Utilization knowledge complicates that benchmark. Chainalysis mentioned adjusted stablecoin financial quantity reached $28 trillion in 2025, with a baseline projection of $719 trillion by 2035 and a catalyst situation approaching $1.5 quadrillion.

As projections, these figures are situation math fairly than proof of future fee flows. Their route adjustments the working query: stablecoins are being evaluated as funds infrastructure, treasury infrastructure, and settlement infrastructure, alongside their position as buying and selling collateral.

The Chainalysis adoption work exhibits why rising markets sit close to the middle of that debate. It ranked India first, adopted by the US, Pakistan, Vietnam, and Brazil, and described adoption as broad-based throughout revenue brackets.

It additionally tied sturdy adoption to on-ramps, regulatory readability, and monetary and digital infrastructure. These are the variables being examined by Pakistan’s banking round and by local-currency stablecoin efforts equivalent to BILS.

The IMF provides the danger facet. Its March paper on stablecoin inflows and FX spillovers finds that stablecoin flows can have an effect on parity deviations, native forex depreciation, greenback premia, and monetary stability.

Put merely, stablecoins change into extra consequential as soon as they begin behaving like a section of the FX market.

That creates the dwell coverage pressure. Native-currency stablecoins may help preserve home items related in on-chain finance. Banking entry can pull VASPs into monitored channels.

Fee integrations can transfer crypto from portfolio publicity to checkout and settlement. Every rail additionally creates new supervisory calls for round reserves, redemption, cash laundering controls, market abuse, and forex stress.

The proof factors to a selected break up. US ETFs and Wall Road adoption have helped financialize crypto by enhancing entry to publicity. The more durable adoption check is going on the place regulators determine whether or not crypto can contact native cash, financial institution accounts, retailers, and FX markets.

That check remains to be early. BILS wants issuance and utilization. Pakistan wants licensed VASPs working via financial institution accounts. Hong Kong’s new licensees want launches. Japan, the UK, and the EU want guidelines that work below market stress.

The UAE wants clear issuer and register mapping. South Korea wants service provider exercise past bulletins.

If these alerts seem, the worldwide crypto map will look much less like a US-led investment-product cycle and extra like a set of regional monetary techniques absorbing crypto below native guidelines. In the event that they fail to seem, the greenback and US capital markets will preserve doing a lot of the work.

The following check is utilization, measured in opposition to consideration.

{kind=link}