JPMorgan inventory has stumbled 15% from its highs, as this high-quality financial institution noticed its valuation stretch. The Every day Breakdown zeroes in.

Earlier than we dive in, let’s ensure you’re set to obtain The Every day Breakdown every morning. To maintain getting our each day insights, all you have to do is log in to your eToro account.

Deep Dive

The 2008 monetary disaster dealt a crippling blow to the US banking business, however the largest gamers emerged bigger and extra dominant than ever. The biggest of all of them is JPMorgan, which instructions a $775 billion market cap. Based in 1799, JPMorgan is a diversified world financial-services agency, with its companies spanning client banking, bank cards, mortgages, funding banking, industrial lending, funds, securities providers, and funding administration for each establishments and people.

The corporate received to its measurement by persistently rising its earnings and income. Whereas JPMorgan’s enterprise skilled some volatility from 2020-22, its progress since has reassured buyers.

Future Development Projections

Development estimates for JPMorgan have been inching larger this 12 months, however nonetheless name for pretty modest progress. In line with Bloomberg, analysts venture the next:

Earnings Development: 5.9% in 2026, 7.9% in 2027, and 9.8% in 2028

Income Development: 5.5% in 2026, 4.7% in 2027, and 5% in 2028

Analysts presently have a consensus value goal of ~$347 on JPM inventory, implying about 20% upside to right this moment’s inventory value.

Wish to obtain these insights straight to your inbox?

Join right here

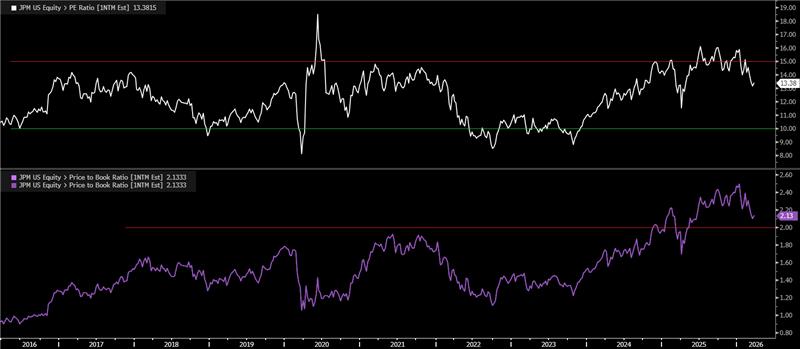

Diving Deeper — Valuation

On Thursday, US regulators proposed easing capital necessities for banks, a transfer that might let the biggest banks maintain about $20 billion much less in capital on common and probably unlock extra lending whereas serving to them compete with private-credit companies. Supporters say it’s going to strengthen conventional financial institution lending, whereas critics warn it may weaken safeguards and spark a broader decline in world banking requirements. General although, it’s being seen as a constructive for banks like JPMorgan, Financial institution of America, Wells Fargo, and Citigroup, amongst others.

Even with that excellent news although, some buyers should have questions on valuation.

On a ahead price-to-earnings foundation, JPM inventory could not look particularly costly, significantly with the S&P 500 buying and selling above 20x earnings. Nonetheless, historical past suggests JPM tends to look comparatively costly round 14x to 15x earnings, whereas dips towards 10x have typically marked extra enticing entry factors. Value-to-book can be an necessary valuation metric for banks, and on that foundation, JPMorgan has hardly ever traded above 1.7x to 2.0x ebook worth — nevertheless it just lately climbed to about 2.5x, its highest stage in at the very least 25 years.

Dangers

JPMorgan is a high-quality financial institution, however it’s nonetheless uncovered to the identical core dangers that drive financial institution shares: a weaker US or world financial system can stress the enterprise. On high of that, non-public credit score is an rising watchpoint — not essentially as a result of JPMorgan sits on the heart of the danger, however as a result of stress in that market may expose points that spill again into broader credit score circumstances. Jamie Dimon has warned there could also be extra “cockroaches” there, which is one other manner of claiming early cracks can reveal deeper issues.

The Backside Line

Financials have been the worst-performing sector to date this 12 months, down about 10% in 2026. In the meantime, JPMorgan has fallen practically 15% from its document excessive in early January.

The pullback has helped ease some valuation issues, and progress expectations have continued to pattern larger, however the inventory nonetheless doesn’t look outright low-cost by historic requirements. Add in lingering macro and geopolitical uncertainty — plus potential spillover dangers in areas like non-public credit score — and it’s simple to see why some buyers should be hesitant to step in aggressively. Conversely, the very best high quality companies hardly ever come at a steep low cost.

Disclaimer:

Please observe that because of market volatility, a number of the costs could have already been reached and situations performed out.

{kind=link}