The entire crypto market cap is down greater than 36% yr over yr, the altcoin advanced sits roughly 45% under its October 2025 peak, and Bitcoin is on track for its worst annual begin in additional than a decade, with capital rotating into AI shares and main IPOs.

Three years of ready for a broad altseason that by no means arrived have left altcoin merchants with fast-decaying narratives, unlock-driven promoting, memecoin rotations that rewarded a handful of early patrons, and rallies that light earlier than most members might measurement in.

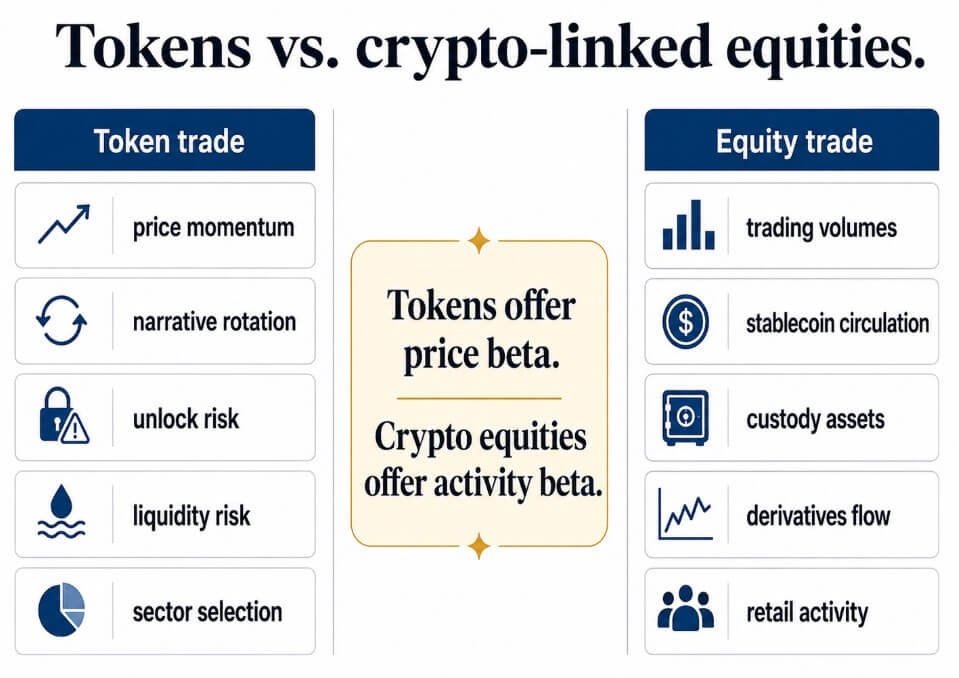

Some traders at the moment are asking whether or not proudly owning the businesses that revenue from crypto exercise is a cleaner commerce than choosing the following token.

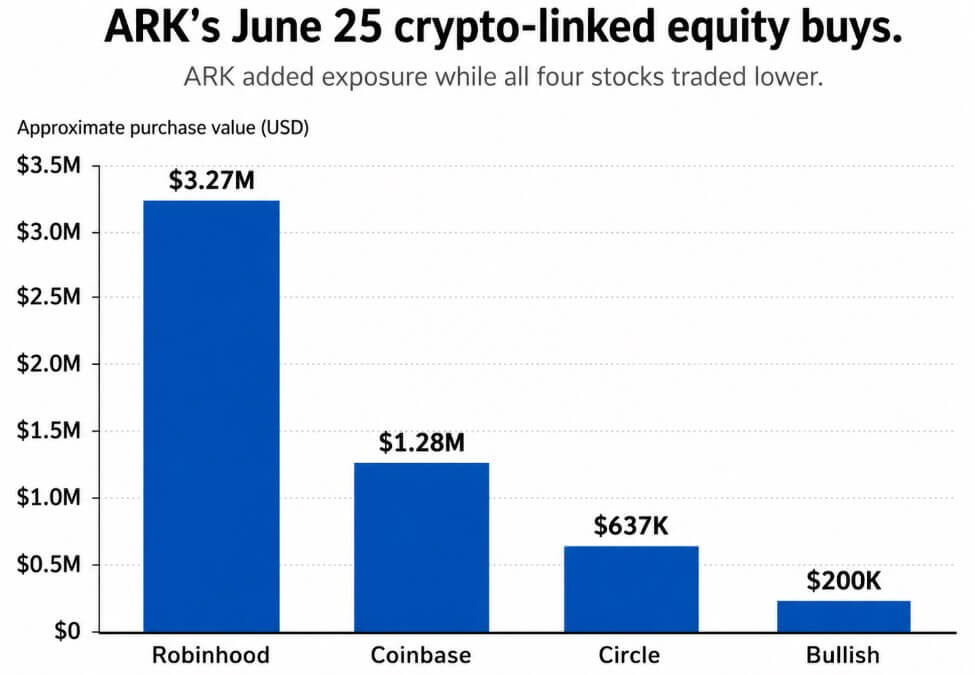

On June 25, ARK’s ETFs purchased roughly $5.4 million in 4 crypto-linked equities, at the same time as all 4 shares traded decrease.

The purchases totaled roughly $1.28 million on Coinbase, $637,455 on Circle, $199,895 on Bullish, and $3.27 million on Robinhood. Cathie Wooden was shopping for into weak point, and the shares she selected are firms that monetize crypto exercise.

Crypto-linked equities give traders publicity to crypto exercise, together with buying and selling volumes, stablecoin circulation, custody belongings, derivatives flows, and retail hypothesis.

Within the sort of low-energy chop that has outlined the previous three years, the 2 bets diverge sharply.

What every title represents

Coinbase’s first-quarter replace reported crypto buying and selling quantity market share at 8.6%, derivatives buying and selling quantity up 169% yr over yr on a trailing-twelve-month foundation, and 12% of worldwide crypto belongings in custody, with greater than 25% of USDC in circulation held in Coinbase merchandise.

These structural positioning numbers replicate what Coinbase collects when volumes return and the way uncovered it’s once they recede.

Coinbase’s transaction income for the interval fell roughly 40% to $756 million, complete income dropped to $1.43 billion from $2.03 billion a yr earlier, and the corporate posted a second consecutive quarterly loss as buying and selling momentum light.

Circle’s USDC circulation reached $77 billion within the first quarter, up 28% yr over yr, whereas on-chain USDC transaction quantity rose 263% to $21.5 trillion.

Complete income and reserve revenue got here in at $694 million, up 20%, pushed by greater common USDC circulation, partly offset by a decrease reserve return price. Stay information as of June 25 confirmed $73.6 billion USDC in circulation.

Circle’s economics run on circulation measurement, reserve yields, and distribution preparations, with altcoin narrative cycles carrying no weight in that mannequin.

Each 100 foundation factors of gross reserve-yield motion on $77 billion in circulation equals roughly $770 million annualized earlier than prices.

CRCL trades as a rates-and-dollar-liquidity wager layered atop a stablecoin adoption wager, with a threat profile formed primarily by rates of interest and regulatory outcomes.

Robinhood’s crypto income got here in at $134 million within the first quarter, down 47% yr over yr, and Robinhood App’s crypto notional buying and selling quantity fell 48%, with a further $42 billion from Bitstamp bringing the whole notional to $66 billion.

Bullish rounds out the basket on the institutional facet, reporting digital asset gross sales of $51.8 billion within the first quarter, adjusted EBITDA of $35.1 million, and 14% open-interest market share in BTC choices in April.

CompanyCrypto exposureWhat has to returnMain riskCoinbaseExchange charges, custody, derivatives, USDC economicsTrading quantity, institutional exercise, retail speculationRevenue falls rapidly when volumes fadeCircleUSDC circulation, reserve revenue, funds infrastructureStablecoin adoption, supportive charges, regulatory clarityLower charges or distribution prices compress economicsRobinhoodRetail crypto brokerage, app-based hypothesis, Bitstamp volumeRetail threat urge for food and crypto notional volumeRetail movement can disappear quick in low-energy marketsBullishInstitutional alternate infrastructure, digital asset gross sales, BTC optionsInstitutional buying and selling demand and derivatives activityInstitutional volumes contract when crypto sentiment weakens

The commerce that follows

Within the bull case, retail hypothesis returns, derivatives exercise recovers, and stablecoin provide continues to develop.

Underneath these situations, exchanges and brokers could reprice earlier than broad altcoin rotation turns into apparent, as a result of transaction income and earnings estimates can reset sooner than token narratives kind.

Coinbase including 10% to its transaction income base of $756 million within the first quarter means roughly $76 million extra per quarter, and that determine reaches $189 million at 25%.

The businesses amassing charges from renewed exercise can transfer ahead with estimates earlier than anybody agrees on which L1, L2, or sector token to personal.

Within the bear case, AI, IPOs, and public-market equities proceed to soak up capital, crypto volumes keep skinny, and the narrative churn that has outlined the previous three years continues.

When exercise fades, public crypto corporations really feel it immediately in income, as Coinbase and Robinhood’s latest outcomes already present.

Circle depends upon USDC circulation holding and reserve yields staying supportive, and Bullish depends upon institutional buying and selling demand that may itself contract when broader crypto sentiment turns.

A protracted crypto winter leaves each one in every of these companies incomes nicely under full capability.

The previous model of the rebound thesis commerce required choosing a token earlier than retail discovered it, accepting the liquidity threat, the unlock schedule, the narrative decay, and the chance that rotation handed by way of a separate sector totally. The fairness model trades token-level upside for a extra legible wager on exercise itself.

Whether or not this cycle’s rotation seems like 2021’s broad altseason or one thing narrower, sooner, and more durable to experience from the token facet is the query Wooden is already positioned on the fairness facet of.

{kind=link}