Fast Breakdown

The digital euro goals to make home and cross-border transactions sooner, cheaper, and safer whereas enhancing monetary inclusion and entry to central financial institution cash for all residents and companies.

Past comfort, the initiative is a strategic transfer by the European Central Financial institution to cut back reliance on non-European fee programs, improve financial coverage management, and shield the euro from geopolitical and monetary pressures.

The digital euro seeks to supply a state-backed different to personal stablecoins and Massive Tech options, fastidiously balancing person privateness, regulatory compliance, and alternatives for fintech innovation.

The digital euro is a proposed Central Financial institution Digital Forex (CBDC), presently being developed by the European Central Financial institution. Its objective is to work alongside money and current digital fee strategies throughout the euro space, not exchange them solely. In easy phrases, the venture is supposed to modernize the best way cash strikes in an more and more digital economic system, whereas giving individuals a public, state-backed possibility as a substitute of relying solely on personal fee platforms. Supporters argue that it may make on a regular basis transactions faster, cheaper, and safer for each customers and companies all through Europe.

Nonetheless, the push for the digital euro is about excess of comfort on the checkout counter. As CBDCs proceed gaining traction world wide, Europe has grow to be more and more depending on non-European fee firms and outdoors monetary infrastructure. That actuality has sparked a wider dialog, and actually, it’s one which reaches past know-how itself. Is the digital euro actually only a instrument for smoother and extra environment friendly funds, or is it half of a bigger technique to defend Europe’s monetary sovereignty in a fast-evolving world economic system?

Fee Effectivity Advantages for Residents and Companies

A core argument for the European Central Financial institution’s digital euro is that it modernizes Europe’s fee system. So how will the digital euro work? It’ll make on a regular basis transactions extra environment friendly, resilient, and accessible for each residents and companies.

Sooner, cheaper home and cross-border funds

The digital euro may drastically cut back the time it takes to ship cash throughout international locations within the eurozone, eliminating delays attributable to correspondent banking networks. Transaction charges would additionally drop as a result of there could be fewer intermediaries and lowered dependence on legacy infrastructure, benefiting each small-scale retail transfers and high-volume enterprise transactions.

Diminished reliance on intermediaries and card networks

By permitting direct peer-to-peer funds between residents or companies, the digital euro may bypass banks and card networks for routine transactions. This reduces prices, lowers counterparty threat, and strengthens European sovereignty over its personal fee ecosystem, which is more and more dominated by world tech and finance firms.

Monetary inclusion and public entry to central financial institution cash in digital kind

In contrast to conventional financial institution accounts, which can exclude some teams attributable to credit score checks or minimal balances, a digital euro pockets may give all residents direct entry to central financial institution funds. This ensures safe, public-backed cash is offered to everybody, together with rural populations, college students, and people underserved by personal banking programs.

Improved resilience of the funds system

A central financial institution–backed digital foreign money would offer a secure fallback throughout technical failures of personal networks or in instances of economic stress. By sustaining a assured, purposeful fee possibility, the digital euro may forestall disruptions that may in any other case paralyze commerce or public providers in emergencies.

Higher transparency and safety in transactions

European Central Financial institution’s digital euro funds may embody cryptographic safeguards and standardized reporting, making it more durable for fraudsters to govern transactions.

Companies may benefit from real-time monitoring, simpler reconciliation, and lowered errors, whereas regulators achieve higher oversight to detect suspicious exercise with out compromising person privateness.

Higher basis for future monetary innovation

With programmable options and public oversight, the digital euro may assist rising monetary applied sciences, reminiscent of automated funds for subscriptions, sensible contracts for commerce settlements, or tokenized property. This creates a dependable infrastructure for innovation with out exposing the system to the dangers of unregulated personal platforms.

Strategic Monetary Independence

The digital euro isn’t nearly pace or comfort; it additionally represents Europe’s bid to say better management over its monetary system and cut back dependence on exterior powers.

Europe’s reliance on non-European fee programs and infrastructure

At the moment, many cross-border funds depend on networks and platforms primarily based exterior the eurozone, exposing Europe to overseas charges, delays, and potential restrictions. By introducing a digital euro, the EU may cut back dependence on these non-European programs, guaranteeing that residents and companies can transact securely inside a homegrown framework.

Digital euro as a hedge in opposition to geopolitical and monetary fragmentation

World tensions and sanctions can disrupt entry to overseas fee networks, leaving European companies susceptible. A European Central Financial institution’s digital euro would offer a secure different, insulating the economic system from political strain and making a monetary instrument that is still absolutely operational no matter exterior disruptions.

Strengthening management over financial coverage transmission

By offering a digital type of central financial institution cash on to residents and companies, the European Central Financial institution can extra successfully implement financial coverage. Rate of interest changes, liquidity injections, or emergency measures will be transmitted sooner and extra uniformly, guaranteeing coverage objectives are met and the euro retains its stability throughout the area.

Enhancing home and regional sovereignty in finance

A extensively adopted EU Central Financial institution digital foreign money would enable Europe to maintain vital monetary knowledge, transaction flows, and foreign money reserves inside its personal jurisdiction. This reinforces autonomy over fee monitoring, regulatory compliance, and systemic threat administration, lowering reliance on overseas oversight or proprietary programs.

Decreasing publicity to overseas foreign money dominance

At the moment, giant world funds usually default to {dollars} or different main currencies, limiting Europe’s means to regulate its personal monetary ecosystem. A digital euro may encourage the euro’s use in worldwide commerce and settlement, boosting the foreign money’s affect whereas lowering dependency on exterior financial coverage.

Constructing a basis for resilient, pan-European monetary infrastructure

By integrating the digital euro into current European fee rails and rising applied sciences, the EU can develop a sturdy, interoperable system. This strengthens cross-border commerce, helps digital innovation, and ensures the eurozone can act cohesively in instances of financial or geopolitical stress.

RELATED:

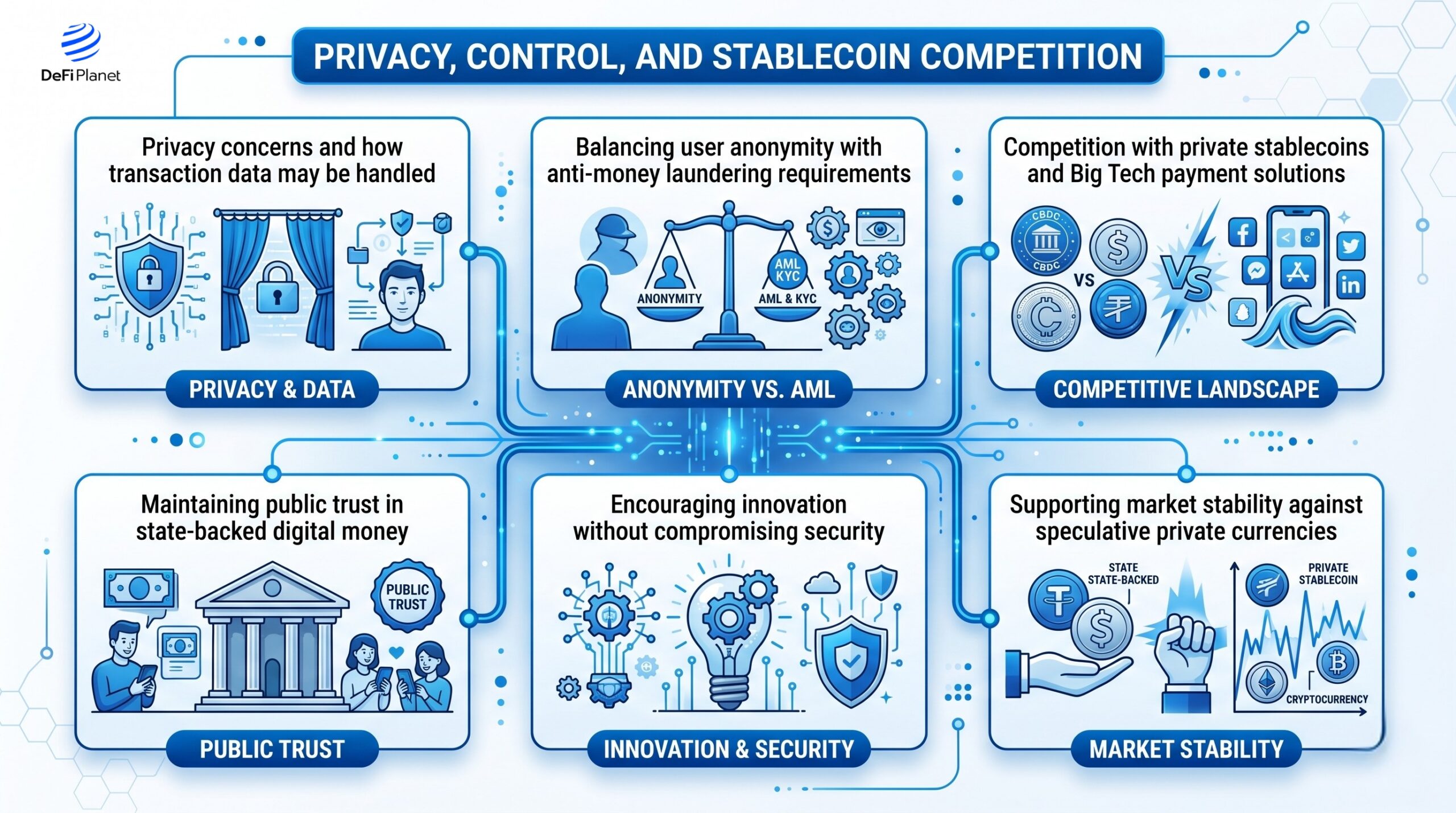

Privateness, Management, and Stablecoin Competitors

The digital euro raises vital questions on who controls monetary knowledge and the way Europe competes with personal alternate options in a quickly evolving funds area.

Privateness considerations and the way transaction knowledge could also be dealt with

A central function of any CBDC is the power to trace transactions, which may conflict with residents’ expectations of economic privateness. The European Central Financial institution’s digital euro should discover methods to guard person data, guaranteeing that spending habits or account balances aren’t unnecessarily uncovered whereas sustaining belief in a government-backed system.

Balancing person anonymity with anti-money laundering necessities

European regulators should stroll a high quality line between safeguarding person privateness and stopping illicit exercise. In contrast to money, digital euro leaves a traceable file, which is important for combating cash laundering, terrorist financing, and fraud, however extreme surveillance may undermine public confidence and adoption.

Competitors with personal stablecoins and Massive Tech fee options

Personal stablecoins and platforms from firms like Apple, Google, or Meta provide quick, handy fee choices, usually with built-in wallets and loyalty options. The EU Central Financial institution digital foreign money goals to offer a public different that ensures sovereignty, retains transaction charges inside Europe, and prevents dependence on overseas or corporate-controlled programs.

Sustaining public belief in state-backed digital cash

As residents weigh privateness in opposition to oversight, the ECB should design the digital euro to be clear and dependable. Clear guidelines on knowledge retention, anonymization, and entry will likely be vital to making sure customers belief the digital euro over personal options or offshore stablecoins.

Encouraging innovation with out compromising safety

To compete with tech-driven alternate options, the digital euro may allow programmable options, micropayments, and integration with fintech apps, all whereas adhering to strict privateness and compliance requirements. This steadiness may spur innovation inside Europe whereas conserving customers’ monetary knowledge underneath public management.

Supporting market stability in opposition to speculative personal currencies

Stablecoins can expertise volatility or fail if not correctly collateralized, risking person funds and systemic stability. A well-designed digital euro affords a safe, absolutely backed different, lowering reliance on probably dangerous personal cash and reinforcing the euro’s function as a secure, reliable unit of trade.

Which Objective Drives the Digital Euro?

The EU Central Financial institution digital foreign money is usually introduced to the general public as a instrument for sooner, cheaper, and extra handy funds, highlighting advantages for on a regular basis customers and companies. Home transfers may settle immediately, cross-border funds could be smoother, and reliance on pricey intermediaries like card networks or overseas processors may lower. These options make the digital euro enticing for residents, providing a contemporary different to money and conventional banking strategies.

Nevertheless, beneath the comfort lies a extra strategic mission: monetary independence and financial sovereignty for Europe. By issuing its personal CBDC, the European Central Financial institution strengthens management over financial coverage, reduces reliance on overseas fee rails, and ensures that the euro stays aggressive in a world monetary system more and more influenced by personal stablecoins and Massive Tech fee platforms.

Though comfort is the public-facing profit, the first driver is sovereignty first, person comfort second. Europe needs a state-backed digital foreign money that safeguards its financial autonomy, protects residents from exterior shocks, and preserves the euro’s world affect.

Conclusion: The Way forward for the Digital Euro

The European Union’s Central Financial institution Digital Forex is shaping as much as grow to be a defining piece of the following chapter in European finance if it sails efficiently. It has the potential to alter how residents, companies, and governments deal with on a regular basis transactions, not simply by making funds extra handy, however by constructing a stronger and extra unbiased monetary system. In some ways, the digital euro represents Europe’s try to cut back its reliance on world card networks, main tech firms, and foreign currency echange that presently dominate giant elements of the fee panorama. That shift may give the area far better management over its personal monetary future.

Trying forward, the digital euro might also reshape cross-border commerce, enhance monetary inclusion, and open the door to new digital providers working on a safe platform backed straight by the central financial institution. And actually, that’s the place issues begin to get actually fascinating. If carried out fastidiously, it may grow to be extra than simply one other fee instrument sitting in your cellphone beside 5 different apps no one remembers downloading. It may evolve right into a core pillar of Europe’s digital economic system.

Nonetheless, the venture’s long-term success will rely upon placing the fitting steadiness between innovation, privateness protections, regulation, and technological reliability. Europe is making an attempt to stroll a reasonably high quality line right here: embracing digital effectivity with out sacrificing public belief or financial sovereignty. If policymakers handle that steadiness nicely, the digital euro may place Europe on the forefront of the worldwide shift towards digital finance. And if not, nicely, even the neatest monetary experiment can find yourself gathering mud like an previous app replace everybody ignored.

Disclaimer: This text is meant solely for informational functions and shouldn’t be thought-about buying and selling or funding recommendation. Nothing herein ought to be construed as monetary, authorized, or tax recommendation. Buying and selling or investing in cryptocurrencies carries a substantial threat of economic loss. At all times conduct due diligence.

Loved this? Bookmark DeFi Planet, discover associated subjects, and comply with us on Twitter, LinkedIn, Fb, Instagram, Threads, and CoinMarketCap Neighborhood for seamless entry to high-quality trade insights.

Take management of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics instruments.”

{kind=link}